Executive Summary

The United States dollar has long been the dominant global currency, and it still is, but for the last two decades, de-dollarization has not only started but is accelerating during the past several years. Once the only superpower, the United States, now faces the rise of authoritarian regimes across globe and in face of BRICS, they try to create and develop some kind of league for authoritarian regimes.

The hegemony of the U.S. dollar had several key drivers, one of which was a long history of sound monetary policy, starting with the Gold Standard and continuing through the Bretton Woods system. Since then, global events have helped the U.S. maintain its dominant currency status for an extended period. The primary reason for this dominance has been the right monetary policies, complemented by factors such as conservative fiscal policies, economic freedom, and strong foreign policy.

However, recent geopolitical tensions—such as Russia's war in Ukraine, terrorist attacks on Israel, and other global conflicts—have accelerated anti-Western actions, including the de-dollarization efforts led by China, Russia, Iran, and other authoritarian states. BRICS countries are actively promoting the use of alternative currencies like the Chinese renminbi to reduce their reliance on the U.S. dollar. There is even ongoing discussion about creating a BRICS currency that could serve as a substitute for the U.S. dollar.

For a currency to achieve global usage as a reserve and trade currency, several factors are essential: historical positive experience, political will, fiscal strength, unity in the case of a common currency, strong property rights, and more. BRICS and its allies currently lack fiscal unity and property rights. To make their currency a viable competitor to the U.S. dollar, they may need to anchor it to gold. If this happens, the process of de-dollarization could rapidly progress, leading to a multipolar monetary system, a development that could signal the end of Pax Americana.

For U.S. policymakers, this shift presents a significant challenge. A decline in dollar dominance would reduce U.S. economic leverage globally, complicate foreign policy tools like sanctions, raise borrowing costs, and limit U.S. influence in institutions like the IMF and World Bank. Most importantly, it would diminish the United States' position as a global superpower. In response, the Federal Reserve and U.S. government must adapt their strategies to maintain leadership in a changing financial and monetary landscape. This may include reforming monetary policy, cutting taxes, balancing the budget, deeper engagement with emerging markets and multilateral institutions. Addressing these trends is essential to preserving the long-term strength of the U.S. economy and its global influence.

Key points

- The dominance of the U.S. dollar has its roots in the Gold Standard.

- The process of de-dollarization has begun and is accelerating over time.

- BRICS countries and their allies are determined to reduce U.S. dominance both politically and economically.

- BRICS nations may introduce a new monetary regime with several realistic scenarios on the table.

- It will be very difficult for the United States to slow, and even more challenging to reverse, the current trend of de-dollarization.

- U.S. policymakers must prioritize reforms in monetary policy and take necessary actions to ensure the U.S. dollar maintains its global dominance.

Table of contents

- Introduction

- Historical Context of the US Dollar Hegemony

- Economic Factors Influencing Dollar Hegemony

- Geopolitical Dynamics and the US Dollar

- BRICS Nations and Their Potential

- Prospects for the Future

- Gradual loss of dominance

- A more rapid decline

- Maintaining the dominance

- Conclusion

- Endnotes

Introduction

Recent years in world politics have been marked by significant changes. The COVID-19 pandemic and Russia's war in Ukraine have accelerated the polarization among nations worldwide. While Western countries previously viewed Russia as a bully-stubborn but still a potential ally, Putin's decision to invade a sovereign nation (the first instance being Georgia in 2008, followed by Crimea in 2014) fundamentally altered this perception. The invasion was going to change European borders for the first time since World War II, solidifying Russia and, alongside China, as a top and imminent geopolitical foe for the West.

This polarization, coupled with poorly managed Western sanctions and delayed, inadequate and late aid to Ukraine, has prolonged the conflict. At the same time, authoritarian regimes have sought to form or expand various alliances. A prime example is BRICS, which includes China, Russia, India, Brazil, South Africa, Iran, Egypt, Ethiopia, and the UAE. While Egypt and the UAE are considered U.S. allies, the other members view Western countries as adversaries.

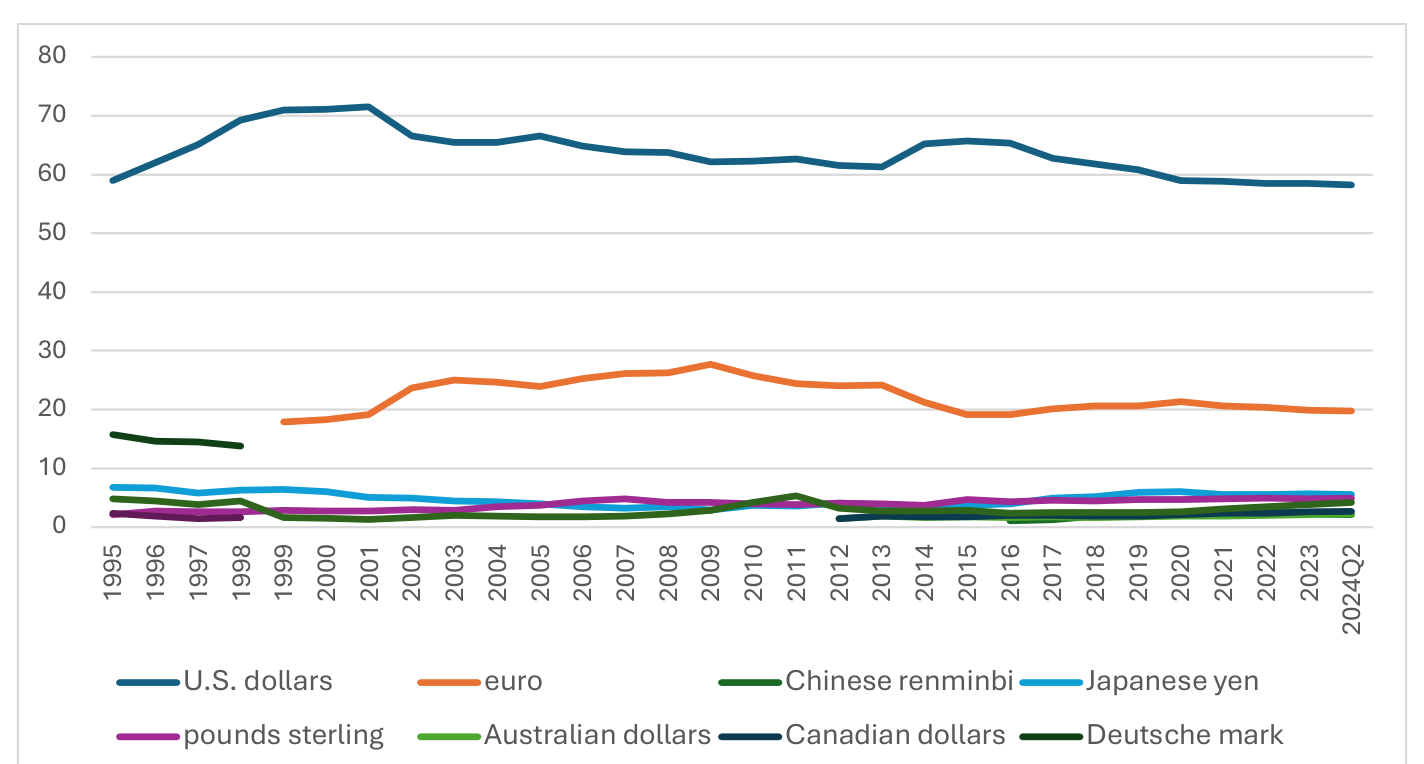

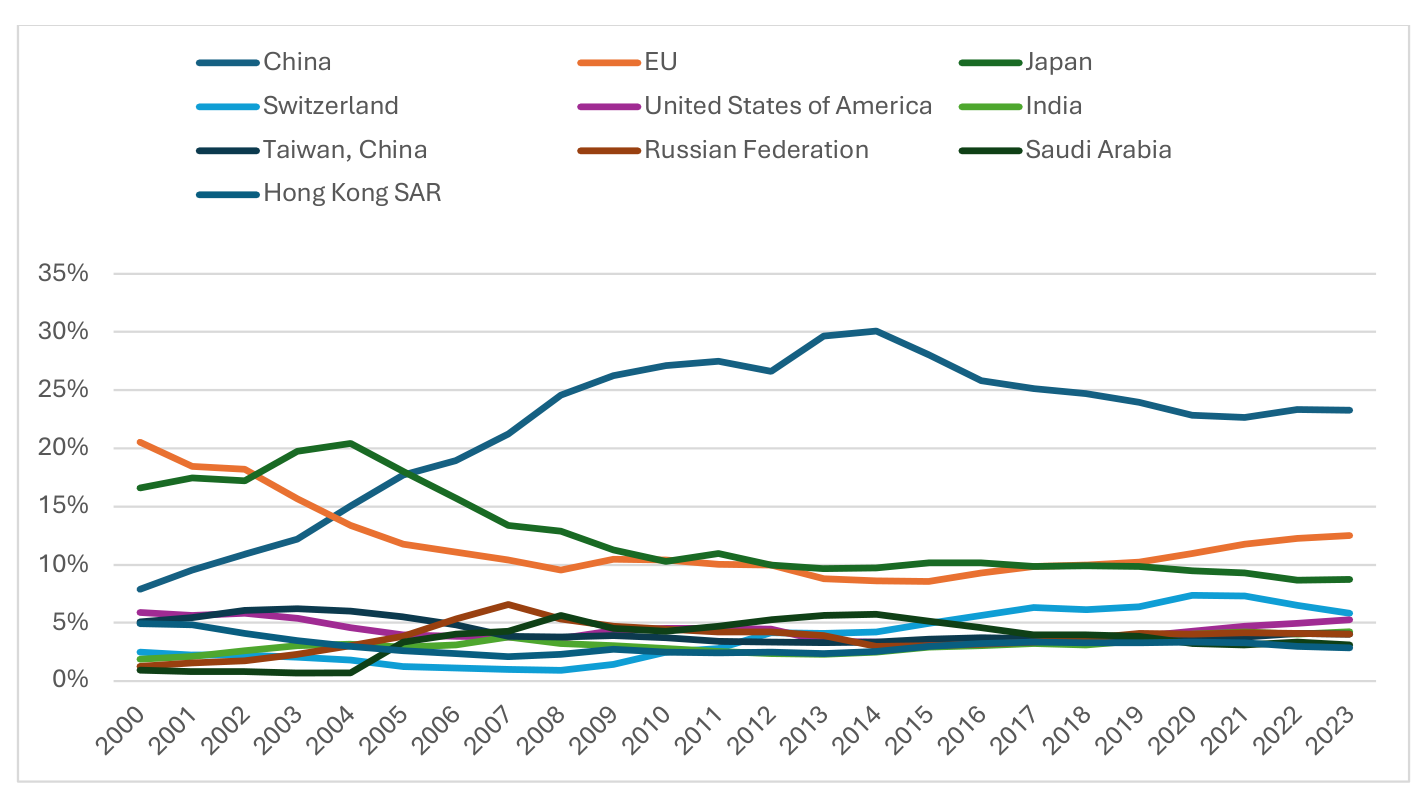

Today, the U.S. dollar constitutes about 58% of all foreign currency reserves and 54% of export invoicing. The euro ranks second, accounting for 20% of currency reserves and 30% of export invoicing. These figures indicate that the U.S. and the European Union are the leading economies in terms of currencies, collectively holding more than 80% of global reserves. However, this situation has evolved over time, and it is essential to consider these changes in context. For example, since the onset of the war in Ukraine, the renminbi has overtaken the dollar as Russia's most traded currency. Currently, the renminbi and gold are Russia's primary reserve assets. Over the past two years, China and Russia have established currency swaps to facilitate trade between them. Additionally, Russia has increasingly utilized the CIPS following the SWIFT ban.

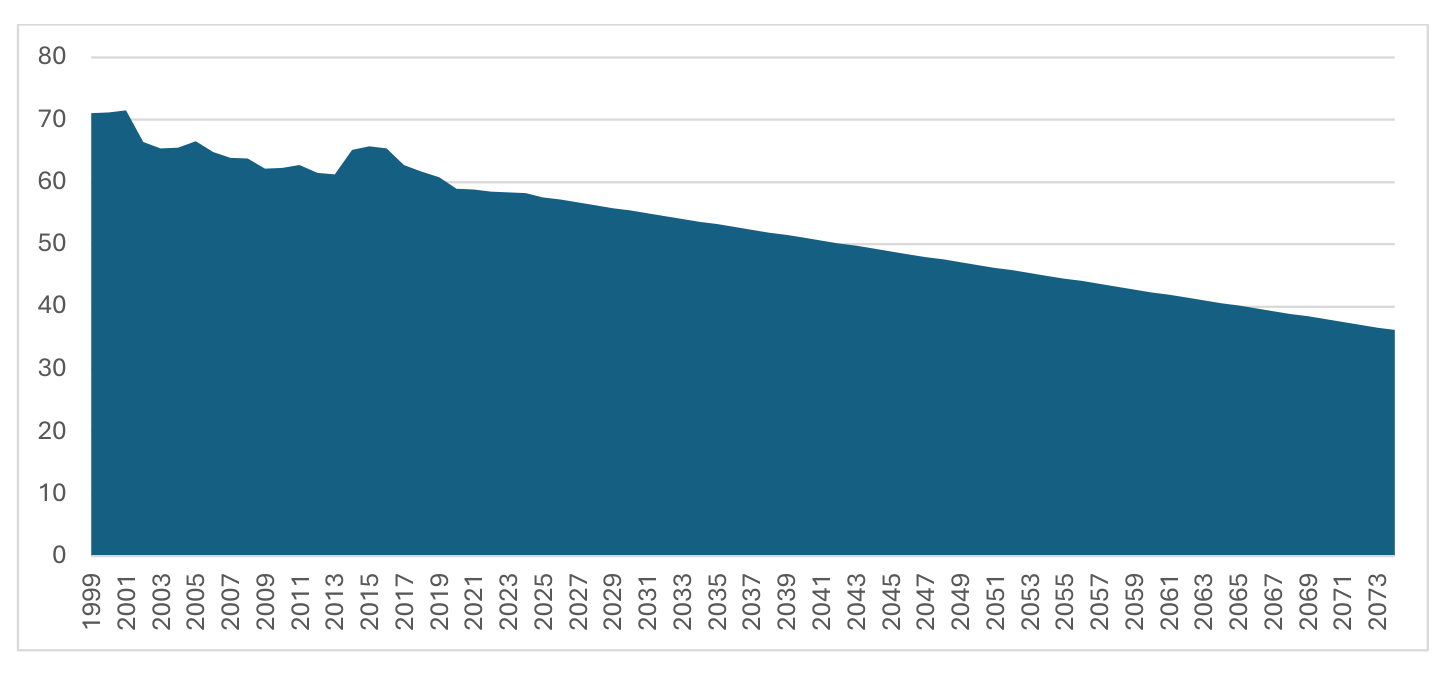

A similar trend is emerging between China and Brazil. De-dollarization has become a key focus for BRICS countries. For instance, in 2013, over 95% of Russia's exports were denominated in U.S. dollars; by 2022, this figure had dropped to less than 40%. Since 2016, the share of U.S. dollars in the global composition of official foreign exchange reserves has declined from 65.5% to 58.2%, down from 72% in 1999. While there has been a slight increase in the euro's share over the past nine years, the last four years have not been favorable for the euro in terms of its share of global currency reserves. Our primary focus will be on the U.S. dollar and its potential competitors, not from traditional political allies like European Union, United Kingdom, Japan and others, but from geopolitical adversaries such as China, Russia, and Iran. We will explore how these nations are working to challenge the dominance of the U.S. dollar in global trade and finance. This analysis will include examining their strategies for reducing reliance on the dollar, such as promoting alternative currencies and forming economic alliances. By understanding the motivations and actions of these countries, we can gain a clearer picture of the evolving landscape of global economic power and the potential threats to the dollar's long-standing hegemony.

Figure 1 shows only allocated reserves, and it is important to mention, that unallocated reserves from 1995 to 2024 decreased from 26% to 7%. Unallocated reserves refer to the portion of global foreign reserves that countries hold without reporting the specific currency breakdown to the IMF. This classification can have several explanations, such as: (1) confidentiality – some countries may choose not to disclose their detailed currency composition for economic or political reasons; (2) incomplete data – the reporting process may not be standardized across countries, leading to the classification of reserves as unallocated; and (3) diverse holdings – some countries hold a mix of reserve currencies in various accounts that are not reflected in the IMF's allocated statistics.

It is reasonable to assume that, in most cases, the currency composition of unallocated reserves closely mirrors that of allocated reserves. Therefore, the significant decrease from 26% to 7% suggests a much higher rate of de-dollarization than what is depicted in Figure 1.

An increasing number of countries are moving away from the US dollar in favor of trading in other currencies. China is actively promoting the use of the yuan in trade, especially with countries in Asia and Africa. Iran, due to sanctions, has sought to conduct trade in euros or other currencies. The same applies to Venezuela. Not only have China and Russia begun using their own currencies, but countries such as Iran and Russia, Venezuela and China, Brazil and China, Bolivia and China, Turkey, Ghana, India, Malaysia, Saudi Arabia, and others are following suit. Countries leading the push for de-dollarization are either members of BRICS or are in the process of joining the alliance.

In this paper our first objective is to evaluate the hegemony of the U.S. dollar (USD), it is crucial to conduct a historical analysis. Currency strength largely depends on monetary policy, so we will examine the policies of the U.S. Federal Reserve over the past 20 years. This period has been particularly challenging for the U.S. dollar, and analyzing global events that have impacted Federal Reserve policy—and therefore the dollar—is essential. Such events may include U.S. involvement in wars, the 2008 Global Financial Crisis, the COVID-19 pandemic, and Russia's conflicts with independent states.

Our third objective focuses on BRICS. It is important to assess the group's potential for expansion, the size of its collective economy, and its stance toward Western countries, particularly the United States.

The final objective is to explore potential policy responses from the U.S. government and the Federal Reserve to maintain the dollar's dominance in the face of rising anti-Western rhetoric, policies, and competition from BRICS nations.

Historical Context of the US Dollar Hegemony

The initial foundation for the U.S. dollar becoming a global currency predates the shifts in global power during World War I and World War II. The gold standard was a key factor in making the U.S. dollar one of the most stable and successful currencies for decades.

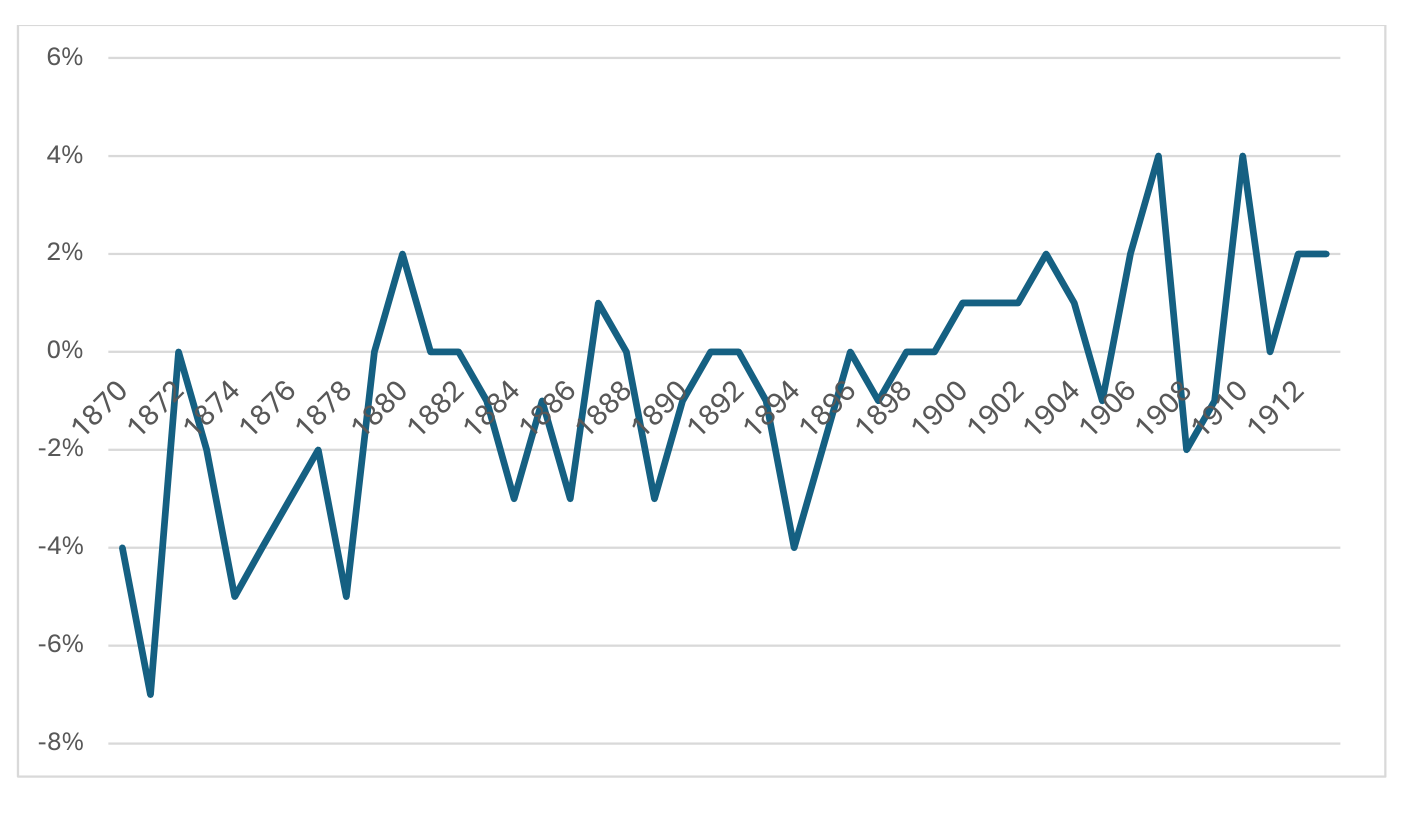

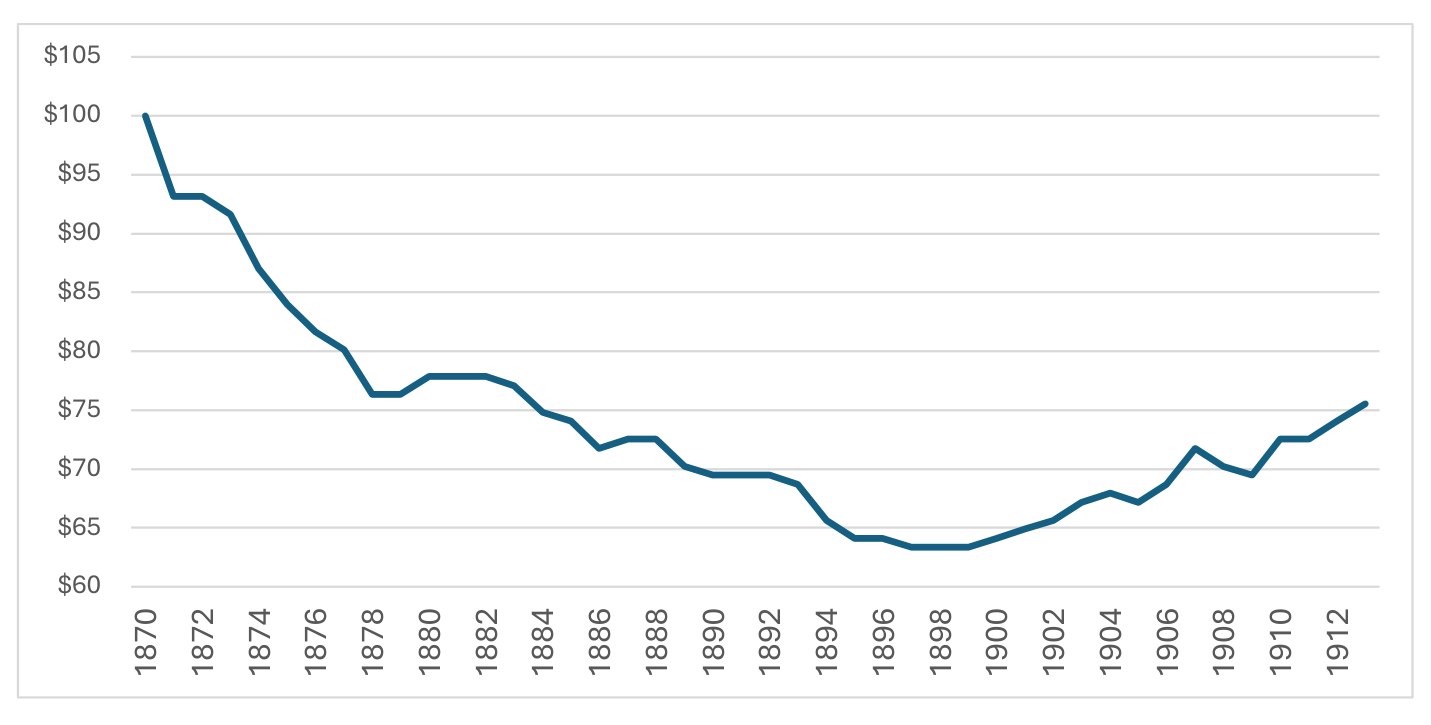

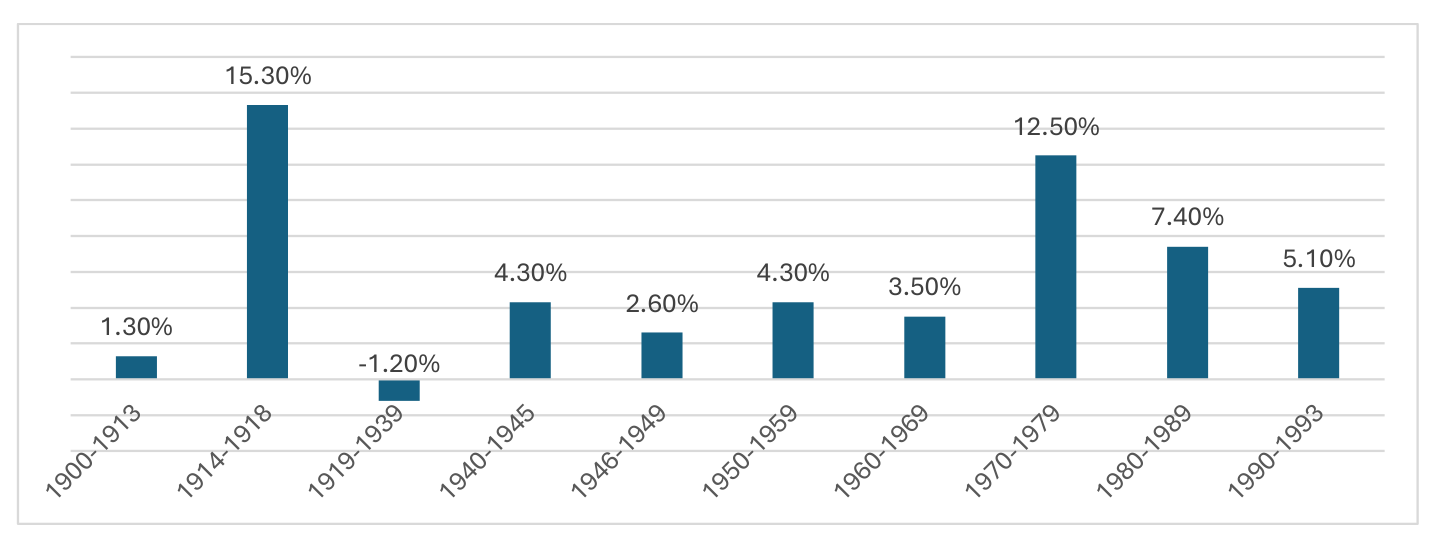

Starting formally in 1870, both Great Britain and, later, the United States adopted the gold standard—a monetary system where every unit of currency was backed by a fixed amount of gold held in reserve. This meant that the money supply was directly tied to the amount of gold reserves, preventing central banks from printing more money arbitrarily. The gold standard was known for creating a sound and stable currency. For example, between 1870 and 1913, the average inflation rate was -0.75%, meaning the value of the U.S. dollar increased over that period, so that by 1913, a dollar was worth the equivalent of 75 cents in 1870. As a result, average prices in the U.S. decreased significantly during this time. In contrast, in just the last five years (2020–2024), prices have risen by 21%, highlighting the stability of the gold standard era compared to more recent inflation trends.

By the onset of World War I, the U.S. dollar had emerged as the world's most stable currency, with the United States positioned as the fastest-growing global power. After both World Wars, political and military dominance further solidified the U.S. dollar's status, as it became the primary currency for international trade. In 1933, The United States along with other countries, officially moved away from the gold standard. There were several formal, but very controversial arguments coming from the government and the main one was to fight deflation with executive order 6102 which prohibited private ownership of gold coins, bullion and certificates. Keynesian economic model needed to increase the public spending.

The next pivotal moment in its rise to becoming the world's dominant currency came with the Bretton Woods Agreement in 1944. Under this agreement, the U.S. dollar was backed by gold, and other currencies were pegged to the dollar. While this initially resembled a gold standard, the U.S. government soon began expanding the money supply, which ultimately contributed to the collapse of the Bretton Woods system in the long term.

Nevertheless, this system formalized the U.S. dollar's global dominance. The final step in its ascent was marked by the collapse of the Soviet Union and the decline of communism, leaving the United States as the world's sole superpower. This ushered in an era often referred to as "Pax Americana." However, this global order now faces significant challenges, primarily from authoritarian governments led by China, Russia and Iran.

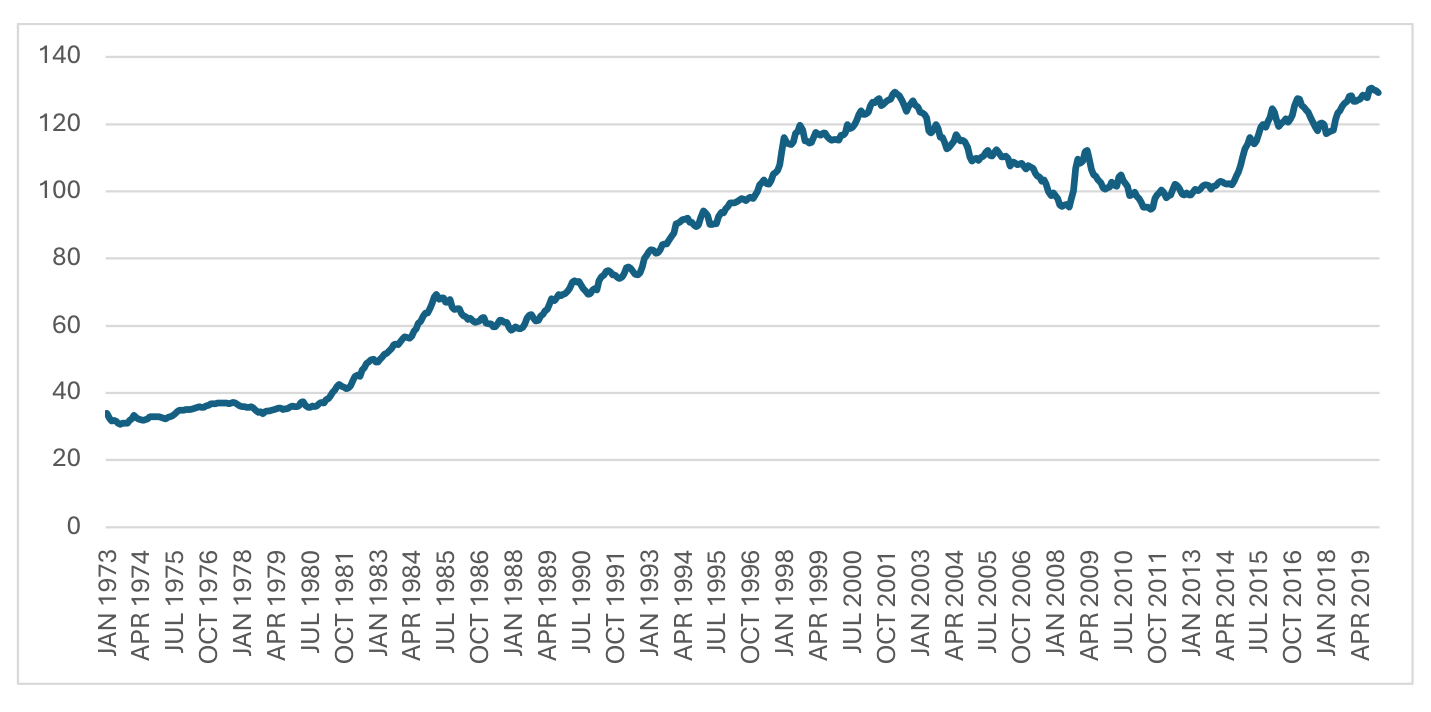

After the Bretton Woods system ended, the U.S. dollar remained the world's dominant currency, but it experienced higher inflation and increased volatility compared to earlier periods. Despite this, the Dollar Index continued to rise until the early 2000s, as the dollar remained the key global reserve currency.

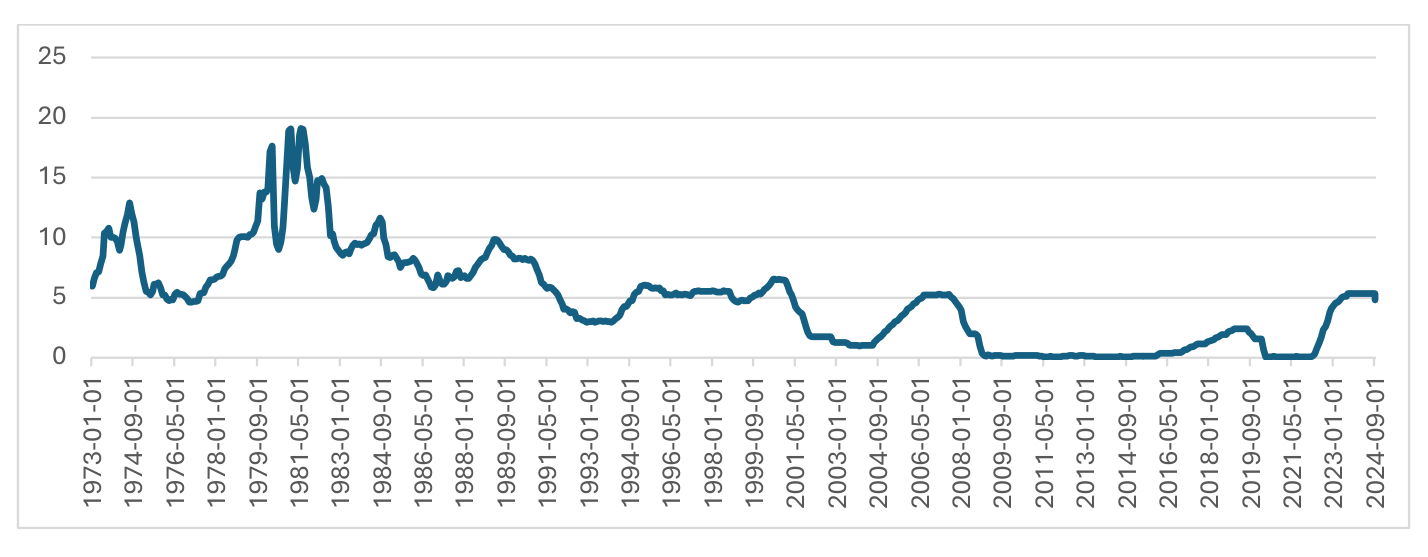

In the 1980s, under Reaganomics, the Federal Reserve raised interest rates, and alongside other economic reforms, the U.S. attracted significant investment and experienced strong economic growth that lasted nearly two decades. These years John B. Taylor calls the Rules-Based Era during 1985-2003, when the primary goal of the monetary policy was price stability and predictable systemic approach with high economic performance. Contrary to the so-called Ad Hoc Era, when monetary policy has been set by the "discretion of authorities" and that contributed to much poorer economic performance. Mainly it was due to Federal Reserve chairman Paul Volcker starting his job in 1979 who conducted the policies of price stability and reversed decades long monetary policy of inflation and later stagflation.

During the years that followed Reagan era, the dollar began to lose value compared to other currencies due to the Fed's low interest rates and expansionary monetary policies. After 2014, dollar regained strength for a short time as the U.S. economy began to recover from the global financial crisis, aided by slightly higher interest rates, but then again de-dollarization process continued.

Economic Factors Influencing Dollar Hegemony

Often economists or other observers forget that the most important thing affecting currency is monetary policy and talk only about trade and political events, but as Milton Friedman stated, "inflation is everywhere and always a monetary phenomenon". So is currency exchange rate, because change in prices is the determinant in formation of exchange rate. There are two opinions about how the US dollar became hegemon currency.

In the fiat money era, the Federal Reserve uses several tools to manage the money supply. These include Open Market Operations, setting Interest Rates, and establishing Reserve Requirements, each of which has its own specific mechanisms. One of the most prominent tools influencing monetary policy is the Effective Federal Funds Rate (EFFR), which has been calculated since 1973. The EFFR represents the cost of borrowing for depository institutions and government-sponsored enterprises. A lower EFFR encourages greater borrowing from the Federal Reserve, which in turn expands the monetary base, ultimately affecting the inflation rate.

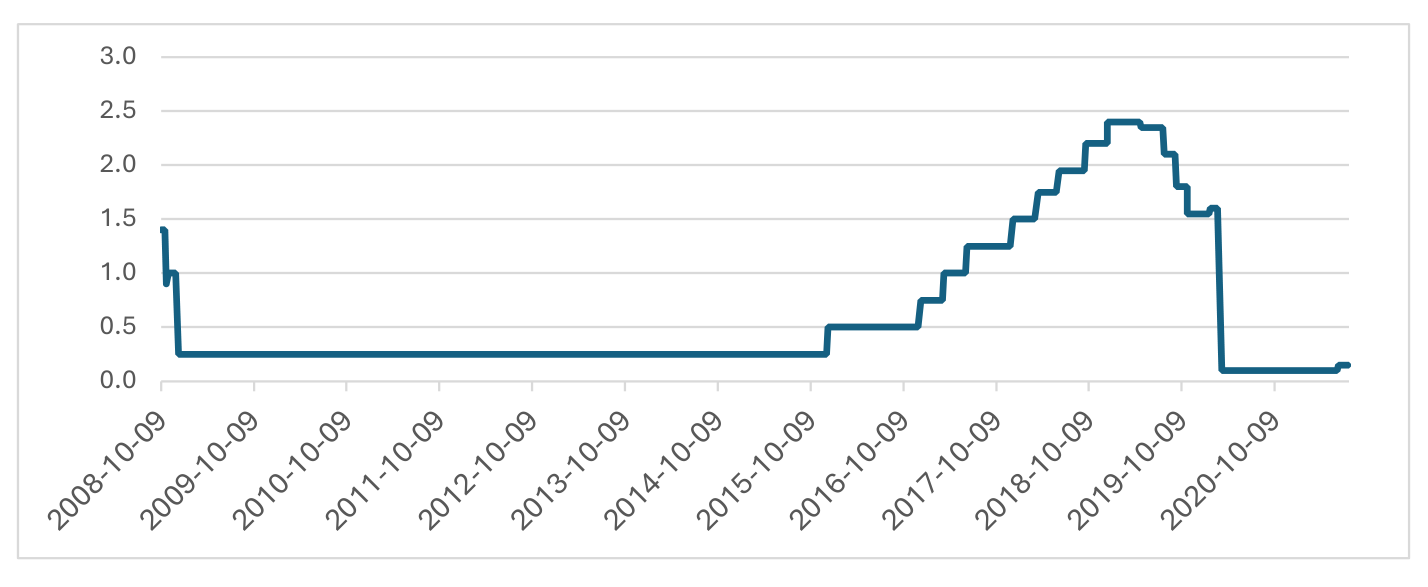

Starting in 1978, the United States implemented a strict monetary policy and maintained high interest rates. After 1989, the Federal Reserve gradually lowered these rates, and by 2009, they had nearly reached zero. Another tool at the Federal Reserve's disposal is the Required Reserve Rate, which mandates that depository institutions hold a specified percentage of each deposit. Since 2020, the interest rate on required reserves has been close to zero, indicating that the Federal Reserve has chosen not to utilize this tool in its monetary policy.

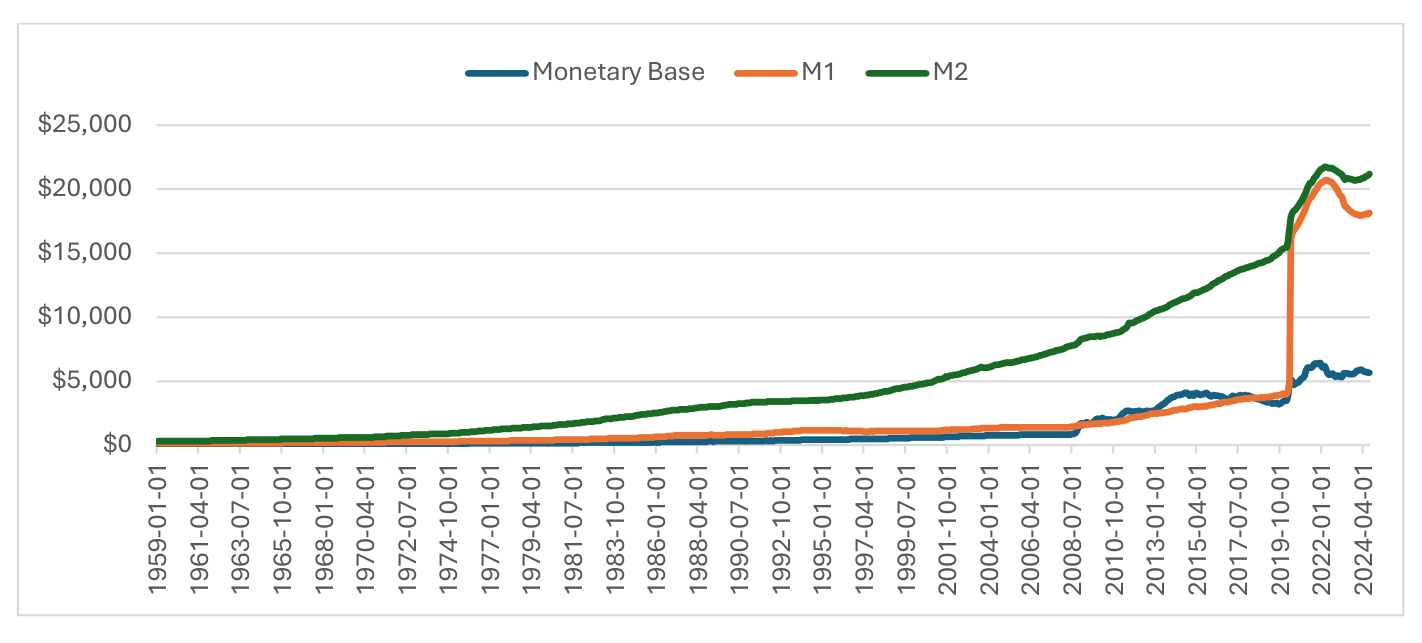

Following the Global Financial Crisis, it became common for governments to implement large economic stimulus packages during times of crisis. This was also the case in 2020, leading to the largest monetary expansion in the nation's history. Between 2020 and 2021, M0 increased by 86%, M1 by 414%, and M2 by 40%.

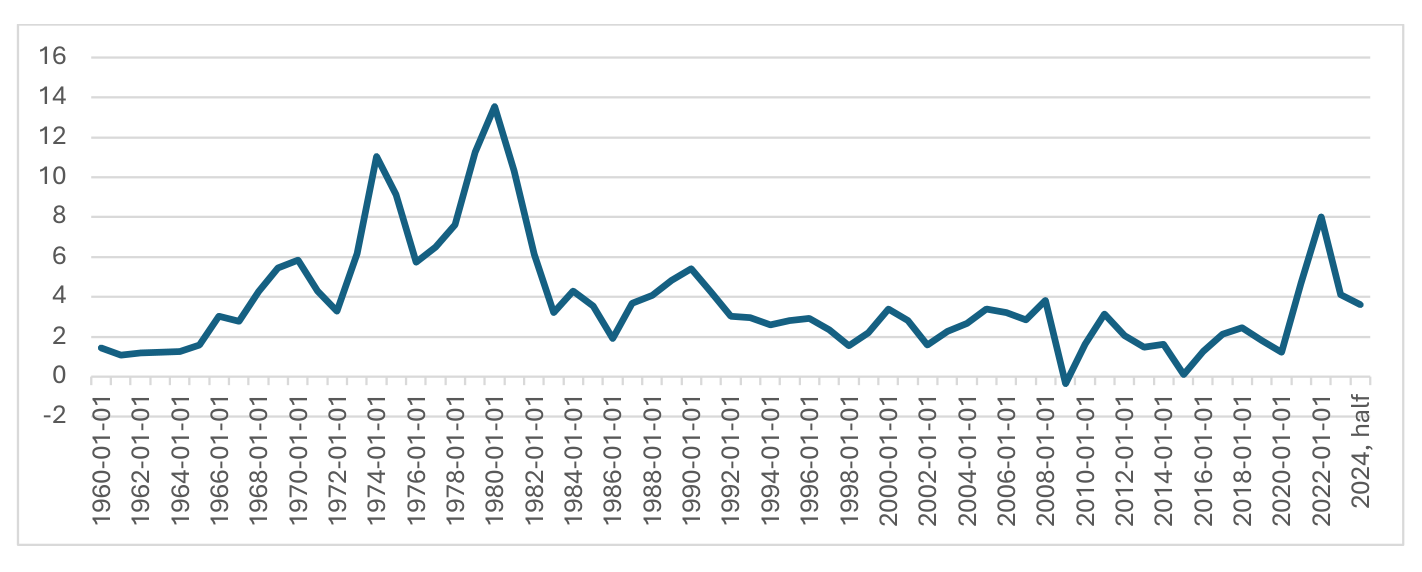

The significant expansion of the monetary base led to the highest inflation rate since the stagflation of the 1970s. Inflation peaked in 2022, reaching 8%, and 2023 saw the second-highest inflation rate in the past 33 years. However, in 2024, inflation began to decline, dropping to 3.6% in the first half of the year and further to 3.2% in August.

The reason for the Federal Reserve inflationary monetary policy lies in its low level of independence. Not only Taylor, but also Allan H. Meltzer states that the Fed independence has varied over the years and in recent decades under political pressure, it was reacting to short-term developments. Monetary policy should be about long-term policies and not short-term interest rates. Also, it is clear that from the creating of the Federal Reserve in 1913, its power grows exponentially and after every financial crisis, new regulations and monetary tools for intervention are adopted.

While monetary policy is the most direct and important factor in discussions of the US dollar's strength and global dominance, economic growth and stability are also crucial for the United States' status as a world superpower. It is important to note that monetary policy influences GDP growth in the medium and long term, but other factors also contribute to economic expansion. One of the most critical factors is property rights. Without democratic institutions, strong and independent courts, and checks and balances, it is impossible to achieve stable, long-term economic growth and societal prosperity. For example, although China has experienced rapid economic growth in recent decades, it is difficult to argue that its citizens enjoy security and prosperity.

One of the key milestones occurred in February 2022, when, after Russia began its war in Ukraine, the United States employed the U.S. dollar as a political tool. In conjunction with other trade, fiscal, and monetary sanctions, the U.S. restricted Russia's access to the Society for Worldwide Interbank Financial Telecommunications (SWIFT). These actions highlight the conflicting roles between governments, even democratic ones, and markets. Governments often exercise monopoly and coercion, while markets are driven by voluntary exchange and decisions based on supply and demand.

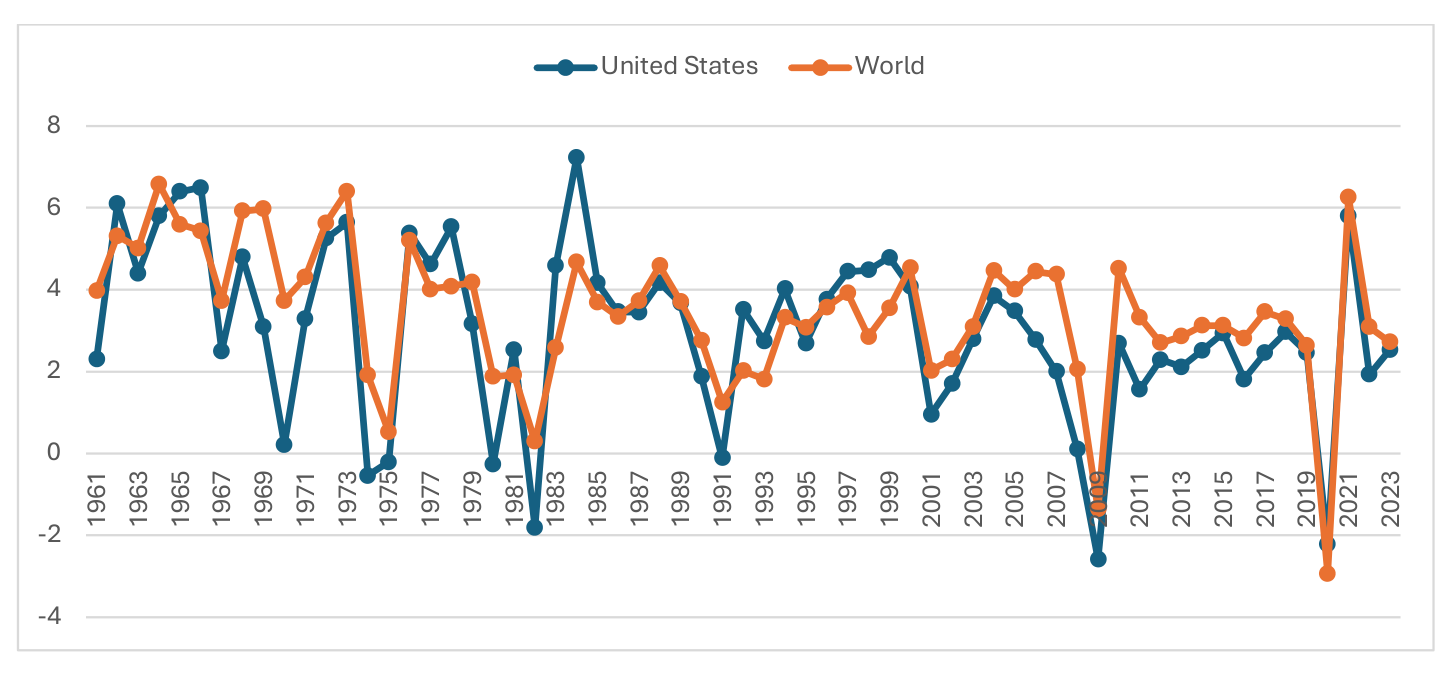

Another important aspect is general economic freedom. According to the Index of Economic Freedom published by the Heritage Foundation, the United States ranks 10th in terms of property rights and 16th in business freedom. In recent years, the US has lost its leading position in economic freedom, although it still holds the longest record of freedom globally. For instance, before the COVID-19 pandemic, the country's freedom score was 76.8, but by 2024, it had dropped to 70.1. In 2006, the score was 81.2, placing the US 5th. In 1995, the United States ranked 3rd, behind Hong Kong and Singapore. These figures indicate that the US has fallen behind other countries in property rights and overall economic freedom for the past decades. This decline in economic freedom has contributed to weaker GDP growth. Since 2000, only one year—2020—saw the US GDP perform as well as or better than the global average, compared to several periods between 1961 and 2000 when the US economy outperformed the global average. Before 1961, the country's performance was even stronger.

No surprise that with these numbers and less successful performance, United States Dollar lost some portion of hegemony around the world. The lesson from the history is that monetary policy is always a crucial component in a long-term nation development and wrong policy may result in catastrophic consequences. Throughout history there are many countries who made such mistakes like Weimar Republic after WW1, Hungary after WW2, Russia and other post-soviet and eastern bloc countries in early 1990s.

The U.S. dollar plays a central role in global finance, being used for borrowing, international payments, and trade. As of 2023, 64% of global debt, 58% of international payments, 54% of trade invoices, and 88% of foreign exchange transactions are denominated in U.S. dollars. Most international trade is settled in dollars, even when the United States is not a party to the transaction. However, in recent years, some countries have begun to move away from trading in dollars. For example, in 2023, China and Brazil completed their first commercial transaction using their local currencies—renminbi (RMB) and reals. That same year, the RMB surpassed the dollar to become the dominant currency in China's cross-border payments. Although the RMB's global market share was only 2.5% in 2023, it grew by 127% over the last decade, which may be a point of concern for the United States.

According to the Atlantic Council, several factors are necessary for a currency to achieve global hegemony: (1) a sizable domestic economy, (2) importance of the economy in international trade, (3) size, depth, openness of the financial markets, (4) convertibility of the currency, (5) use of the currency as a currency peg or anchor and (5) stable domestic macroeconomic conditions and policies. The United States has fulfilled all these criteria for decades and is expected to continue doing so. However, rising concerns about the RMB and other currencies from BRICS nations (Brazil, Russia, India, China, and South Africa), as well as countries seeking BRICS membership, present a challenge. For instance, China has a large domestic economy, and when combined with other BRICS nations, their collective economic size could surpass that of the U.S. Similarly, the importance of these economies in global trade is increasing, with more countries opting to conduct trade without using U.S. dollars. This has led to growing demand for an alternative, "neutral" single currency.

The benchmarks for currency dominance: convertibility, use as a peg, and open financial markets—remain largely the domain of Western nations, posing significant challenges for BRICS countries. Another challenge is maintaining stable macroeconomic conditions, which can be difficult for authoritarian regimes. However, there is speculation that these countries may attempt to overcome these hurdles through initiatives let's call an "Asian Gold Standard," where BRICS nations could issue a currency backed by gold, or an "Asian Bretton Woods system," in which the RMB could be backed by gold and used as a reserve currency by other countries.

De-dollarization has already begun, with many authoritarian nations in Asia and Africa seriously pursuing geopolitical unity as an alternative to the Western order. For them, it is a matter of survival, as history shows that Western countries consistently support democracy and human rights, making authoritarian regimes vulnerable in the long run. As Peter C. Earle states: "The dollar, in some shape or form, will likely be around for a long time. Perhaps very long. But by weaponizing dollar dominance and permitting expanding mandates to disorient US monetary policy, the dollar's fate as the lingua franca of world commerce over the long haul may already be sealed." Russia's invasion of Ukraine accelerated this process, serving as a wake-up call for European nations and the United States. Poorly managed sanctions on Russia had minimal impact on its economy but contributed significantly to the de-dollarization and anti-western movement.

Geopolitical Dynamics and the US Dollar

As previously mentioned, U.S. dollar hegemony must be understood through the lens of free-market forces, the government's role in fostering economic stability, and its promotion of international political and economic cooperation. Economic freedom, individual rights, and sound money, underpinned by the gold standard, propelled the United States to become the world's leading economy and superpower. The U.S.'s pivotal role in winning World War II, followed by the Bretton Woods Agreement and the global collapse of communism, cemented the dollar's dominance on the world stage.

In recent years, the second key driver of de-dollarization—after monetary policy—has been geopolitical dynamics. After the collapse of the Soviet Union, it appeared, as Fukuyama suggested, that "history was over" and the United States would remain the global hegemon for an extended period. However, by the early 2000s, it became clear that Western civilization was facing new threats. These threats included terrorism and the rise of authoritarian regimes, led by the Russian Federation and China. Vladimir Putin's ambition to rebuild the Soviet Union, coupled with China's growing economic influence and aspirations in Asia and Africa, signaled significant challenges to U.S. global leadership.

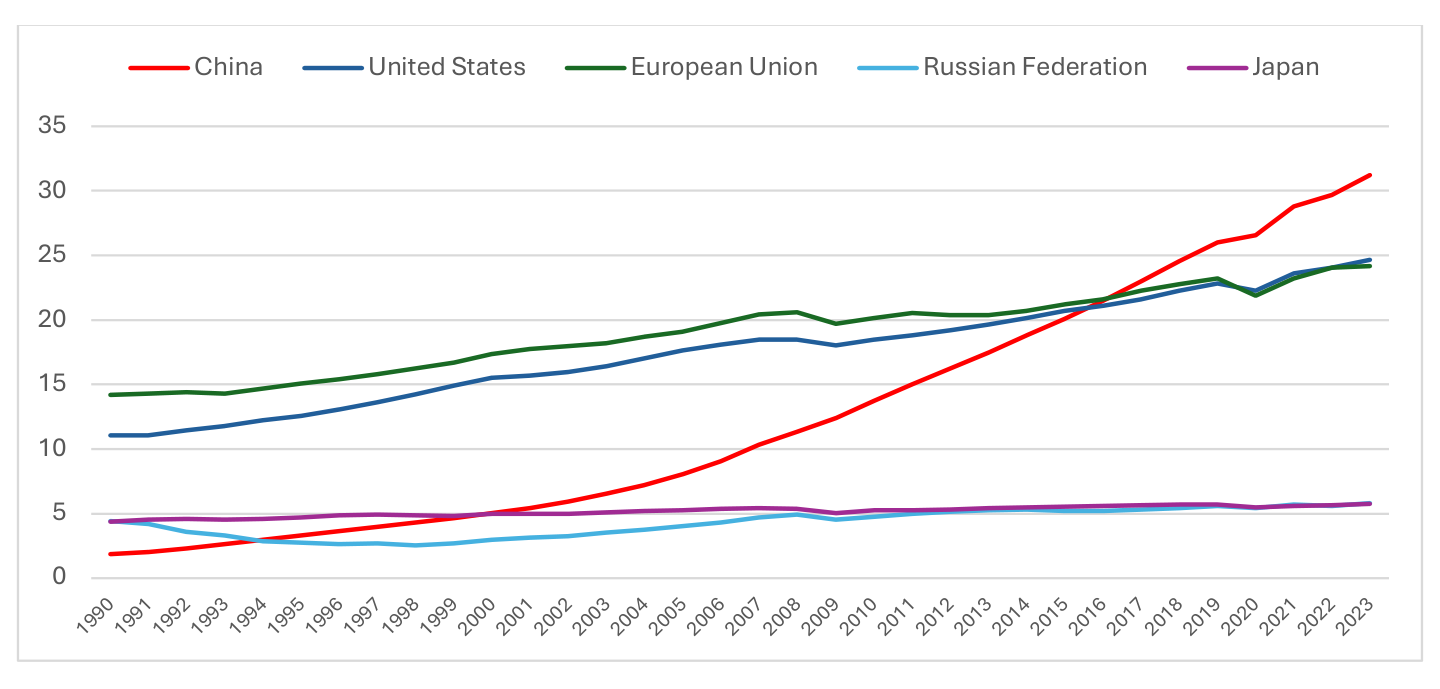

China's growth since the 1990s has been remarkable. In 2001, it surpassed Japan, and by 2017, it overtook the United States in terms of purchasing power parity (PPP). While the U.S. economy remains 54% larger in nominal terms, comparing economies based on PPP provides a more accurate measure of their relative size.

It is important to note that per capita GDP differs significantly between the two countries. In terms of PPP, the U.S. per capita GDP stands at $81,695, whereas China's is $24,557. The gap is even wider in nominal terms, with the U.S. at $81,695 compared to China's $12,614. However, GDP per capita alone is not a sufficient metric to evaluate the quality of life for the average citizen. Other factors, such as the rule of law, property rights, and access to goods and services, must also be considered.

The Chinese economy is undeniably large. While the country may lack key elements such as property rights, institutional checks and balances, and other factors essential for attracting investment and immigrants, these are primarily vital for democratic nations. In authoritarian systems, there is no true concept of private investment, as the state controls businesses, and consequently, every currency unit is subject to government control. This allows authoritarian regimes to cooperate economically and support each other whenever needed.

Although, like communist systems, this model is inherently inefficient, costly, and unstable in the long run, history has shown that authoritarian leaders can not only maintain their power but also expand their influence on other countries. Therefore, it is unwise to rely solely on the assumption that inefficient forms of government will collapse on their own.

The first major geopolitical shift is linked to China's rise as a global power. In the economic competition between the United States and China, becoming the world's largest economy is a symbolic milestone. While it is widely acknowledged as inevitable—given that China's population is 4.2 times larger than that of the U.S.—the moment when China surpasses the U.S. economy for the first time in modern history is still noteworthy.

Additionally, China's Belt and Road Initiative (BRI) is a massive undertaking that will further solidify its position as an economic superpower and hegemon in Asia and Africa. The BRI encompasses extensive infrastructure projects, such as the New Eurasian Landbridge, the China-Mongolia-Russia Corridor, the China-Indochina Corridor, the China-Bangladesh-India Corridor, the China-Pakistan Corridor, the China-Central Asia-West Asia Corridor, and the Maritime Silk Road. These projects will significantly increase trade and cooperation among Asian countries.

While increased trade typically leads to greater prosperity and peace among nations, it also grants China considerable influence, furthering its hegemonic power. China's dominance has also expanded through technological competition. Companies like Huawei and TikTok exemplify China's growing influence in many parts of the world.

The second event that shaped global geopolitical dynamics was U.S. foreign policy. Under President Obama, several initiatives had far-reaching consequences. Efforts such as the "Reset" with Russia and the withdrawal from the Middle East contributed to the rise of ISIS, the Syrian crisis, and allowed Russia and China to expand their influence in the region. Iran also grew stronger following the Iran Deal. During Obama's tenure, countries like Hungary, Greece, and Italy, among others, fostered closer ties with authoritarian Russia. Meanwhile, Germany, France, and much of Europe became increasingly dependent on Russian oil and gas. Pro-Russian forces even won elections in Ukraine and Georgia.

The Trump administration continued this trajectory, though its focus shifted more towards confronting China rather than Russia. The U.S.-China trade war during this period further weakened the U.S.'s global economic dominance and contributed to a gradual erosion of its hegemony.

Another significant geopolitical shift, as mentioned above, was the resurgence of Russia. In the early 2000s, Russia implemented strict monetary policies, maintained low taxes, and followed fiscal conservatism. Additionally, the country expanded its oil and gas exports, not only to Europe but to other regions as well. These policies facilitated stable economic growth, a military revival, and, in 2008, Putin launched a full-scale war in Georgia. Russia still occupies over 20% of Georgian territory. With a weak U.S. response and Obama's "Reset" policy, Russia was emboldened to annex Crimea in 2014. Even this did not serve as a sufficient wake-up call for Western countries, and the severity of the situation became evident when Putin initiated another full-scale war, this time in the heart of Europe—Ukraine.

The United States and its Western allies responded with sanctions against Russia and military aid to Ukraine. However, both were poorly managed, largely due to bureaucracy and political polarization in elites within the U.S. and the EU. Military assistance often arrived late, after Russia had already made significant advances, and the same was true for sanctions. Furthermore, in many cases, sanctions proved ineffective. Russia continued to procure goods and services through non-sanctioned countries, particularly China. This situation has only strengthened the relationship between Russia and China, turning China into Russia's closest partner.

Since 2022, numerous sanctions have been imposed on the Russian Federation. The United States, European Union, and other Western allies introduced a wide range of sanctions, targeting Russian oligarchs and politicians, and placing trade bans on certain materials, electronics, and related goods that could be used in the war against Ukraine. In 2022, the Central Bank of Russia lost access to over $400 billion in foreign reserves. Additionally, in 2023, G7 countries froze more than $335 billion in Russian assets held abroad. Russia was also banned from the SWIFT international payment system. The only significant reserve commodity Russia retained was its gold reserves, totaling $130 billion.

The United States and Canada banned all oil and gas imports from Russia, while the European Union significantly reduced its dependence on Russian energy. Hungary, which is considered a key Russian ally by many political authors, was the primary reason the EU did not fully halt energy trade with Russia. However, the EU plans to completely end its reliance on Russian energy by 2030. One of the most impactful sanctions appeared to be the G7's decision to cap the price of Russian oil. This measure initially worked, maintaining oil prices around the cap and reducing Russia's oil revenues in 2023. Unfortunately, by 2024, the trend had reversed.

China, India, and Turkey are the primary buyers of Russian coal, crude oil, and oil products. Within the European Union, Hungary and Slovakia are the main consumers of Russian pipeline gas and crude oil. These countries are considered Russian allies within the EU due to their pro-Russian and anti-Western governments.

The sanctions imposed on Russia have pushed it closer to other authoritarian regimes, such as China and Iran. BRICS countries have become increasingly active in transforming their geopolitical alignment into a more pragmatic unity, aimed at countering Western influence.

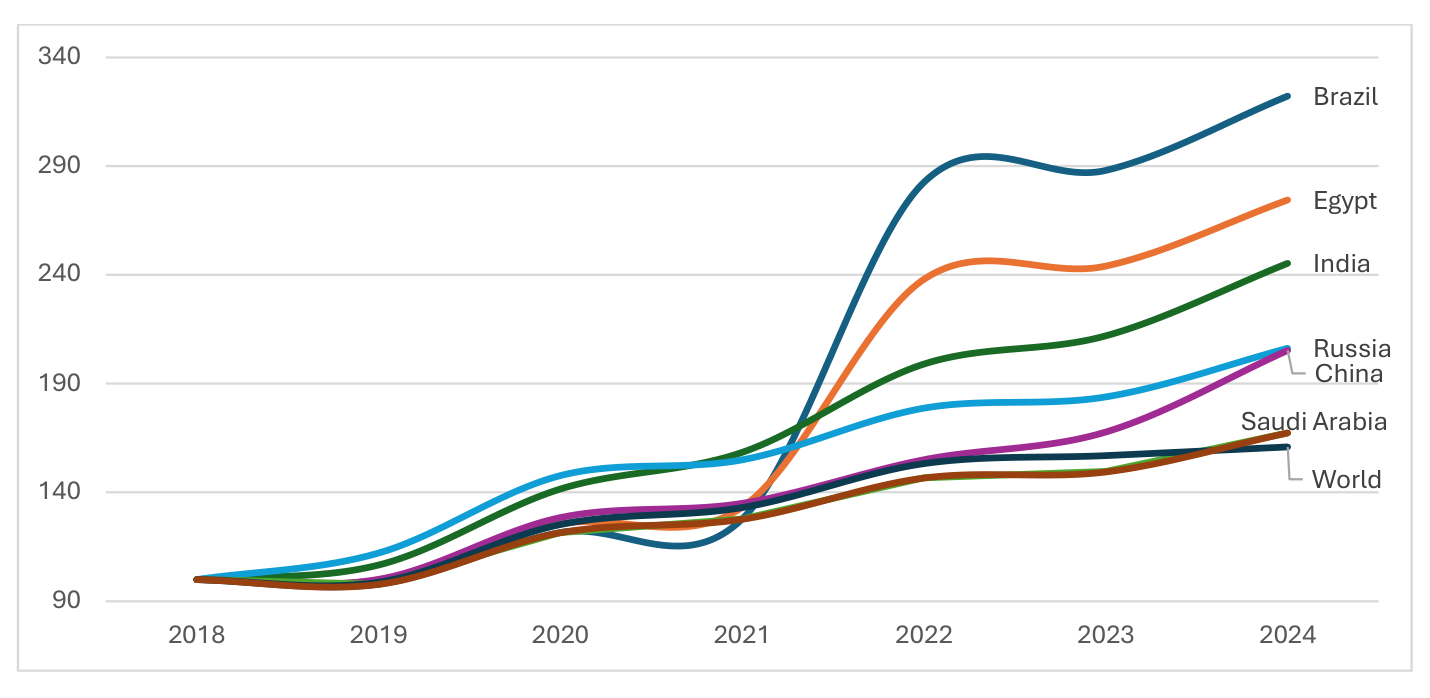

The sanctions also underscored the critical importance of gold as the most reliable and stable commodity a country can hold as a reserve. After Western nations imposed sanctions on Russia, freezing assets like foreign currency reserves and blocking access to international financial systems, gold stood out as the only asset they could neither seize nor prevent Russia from utilizing. This demonstrated gold's unparalleled value as a hedge against sanctions and geopolitical risks, offering financial security in times of heightened global tension.

As a result, many authoritarian regimes, particularly BRICS countries, have increasingly turned to gold, bolstering their reserves as part of a broader strategy to insulate their economies from potential external pressures. The move reflects a growing realization that in a world where economic sanctions are increasingly used as a geopolitical tool, holding substantial gold reserves provides a form of economic sovereignty. Countries are, therefore, prioritizing gold to reduce reliance on the U.S. dollar-dominated financial system and to safeguard their financial stability in the face of potential future sanctions or global market disruptions.

On its own, gold has many advantages. First of all, it guarantees stable currency and low or no inflation. Under the gold standard, the value of currency is directly linked to a fixed amount of gold that lowers inflation. Figure 2 and 3 showed us how the gold standard lowered prices in the United States. Second advantage is trust. Trading partners are more confident in doing business with a country, who has its currency backed with gold and therefore has very low volatility risks. This also leads to an increased overall economic confidence that can play a crucial role in attracting foreign direct investments. One more advantage improved relationship between countries because of the balancing the trade between them. Under gold standard, countries cannot manipulate currency and also their trade deficit and surplus tend to decrease in a medium and long run. Another very important advantage is that gold standard leads to a global standardization. It is the perfect way out for example for BRICS countries to adjust their currencies to each-other, introduce single currency backed by gold or use Renminbi as an anchor currency therefore significantly reduce their dependence on U.S. dollar.

China is a dominant gold reserve holder from 2005, when it surpassed Japan. Currently China holds approximately 23% of world's gold reserves, while in 2001 it held less than 8%. In 2000 Japan had 17% of the world gold reserves, while current EU countries about 21% and now they have 9% and 13% respectively. Saudi Arabia more than tripled its share, Russia quadrupled, and India doubled their share in global gold holdings. China, Russia, Saudi Arabia and India are BRICS countries and in total they have 35% of total global gold reserves, with Brazil and Hong Kong – 40%, while EU, Japan and the United States have only 27%.

In recent years, BRICS countries have not only been actively purchasing gold, but they are also considering adopting gold as a reserve currency. For instance, the Atlantic Council notes that Russia and China are moving toward gold-backed currencies. De-dollarization was one of the key topics discussed at the 2023 BRICS Summit in South Africa. However, differences among the countries delayed the creation of a single currency. During the summit, Brazil's President Luiz Inacio Lula da Silva stated, "The creation of a currency for trade and investment transactions between BRICS members increases our payment options and reduces our vulnerabilities." During a visit to China, he also remarked, "Why can't we conduct trade using our own currencies? Who decided that the dollar should be the dominant currency after the disappearance of the gold standard?" This clearly signals that Brazil, alongside Russia, supports the idea of a single currency. Russian embassy in Kenya also declared that "the BRICS countries are planning to introduce a new trading currency, which will be backed by gold". Alexander Babakov, deputy chairman of Russia's State Duma said in Delhi that Russia is now spearheading the development of a new currency under BRICS umbrella. During 2024 BRICS summit in Kazan, Russia, Indian Prime Minister Narendra Modi welcomed the efforts to increase financial integration among BRICS countries, trade in local currencies and smooth cross-border payments will strengthen our economic cooperation. During the summit, Russian State Duma Speaker Vyachaslav Volodin also wrote in his Telegram channel that "The time of hegemony of Washington and Brussels is passing".

In contrast, South Africa's Finance Minister pointed out that establishing a single currency would require a unified central bank, which would result in a loss of monetary independence—something no country is ready for.

These differing perspectives underscore the challenges BRICS countries face in adopting a unified currency. The political and economic coordination required, alongside concerns over losing monetary independence, means that a single currency remains a distant goal. In the meantime, more practical alternatives could include individual countries re-adopting the gold standard, linking their currencies to gold, or pegging their currencies to the Renminbi, which could itself be backed by gold. These options would provide a gradual shift toward a more gold-based system without the complexities of creating a shared BRICS currency.

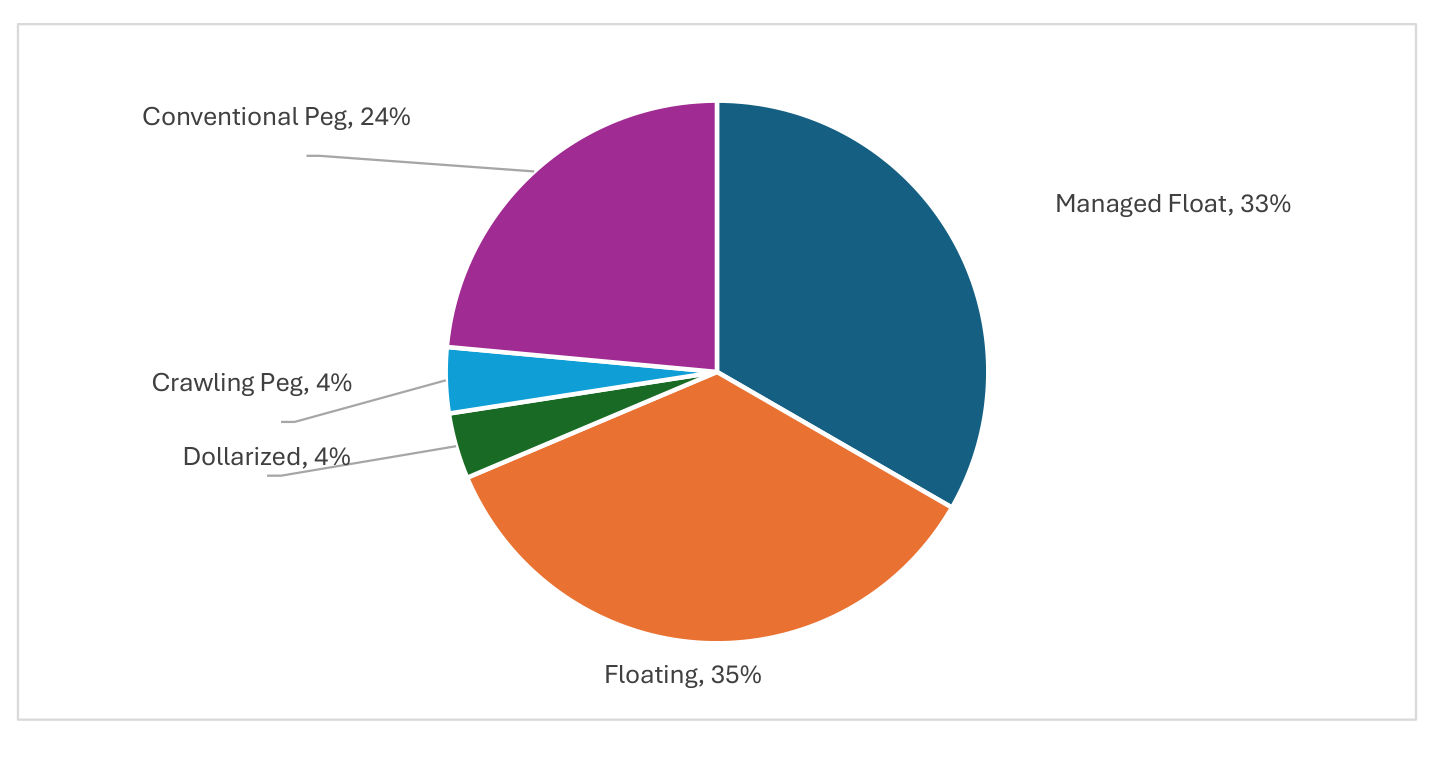

While South Africa's Finance Minister's concerns are valid, it's important to note that not all BRICS countries and potential members have floating exchange rates and, therefore, independent monetary policies. For example, the United Arab Emirates' currency is pegged to the U.S. dollar, as are the currencies of Cameroon, the Central African Republic, Senegal, Iraq, Saudi Arabia, Yemen, and others. Additionally, El Salvador and Zimbabwe are dollarized, which goes beyond lacking independent monetary policy—they are directly dependent on the Federal Reserve's monetary policy.

Figure 13 shows that only 35% of countries have an independent monetary policy. The majority of other countries have currencies that are either fully pegged or managed according to global basket currencies like U.S. dollar, euro, Swiss franc, etc. This suggests that most countries would likely be willing to either peg their currency to the Renminbi or gold or adopt a new BRICS single currency if they are considering joining BRICS and reduce their economic dependency on western countries.

BRICS Nations and Their Potential

BRICS, founded in 2009, is an acronym for its five initial member countries: Brazil, Russia, India, China, and South Africa. Initially, BRICS represented nations with emerging economies, large territories, substantial populations, and significant market potential. Over time, the organization has come to symbolize an alliance of authoritarian governments aimed at reducing Western hegemony and promoting a multipolar world order.

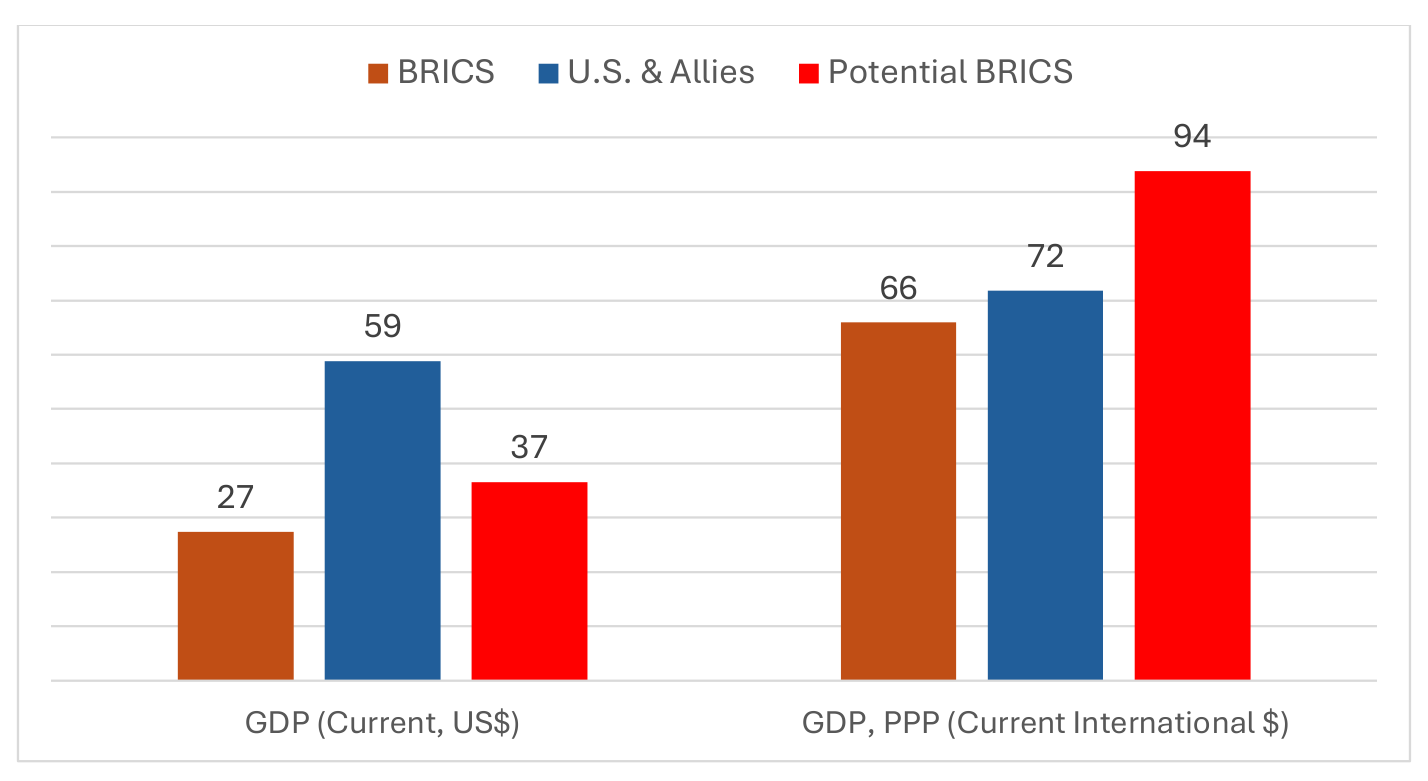

The BRICS countries represent 45% of the world's population and 45% of its land area. In terms of global wealth, their combined GDP amounts to $27.4 trillion (in current U.S. dollars), accounting for 26% of global GDP. When measured by purchasing power parity, BRICS' GDP rises to nearly $66 trillion, representing 35.7% of the global economy. These figures are significant, and BRICS has substantial potential to challenge the unipolar world order, potentially creating greater geopolitical issues than those posed by individual nations such as Russia, China, and Iran.

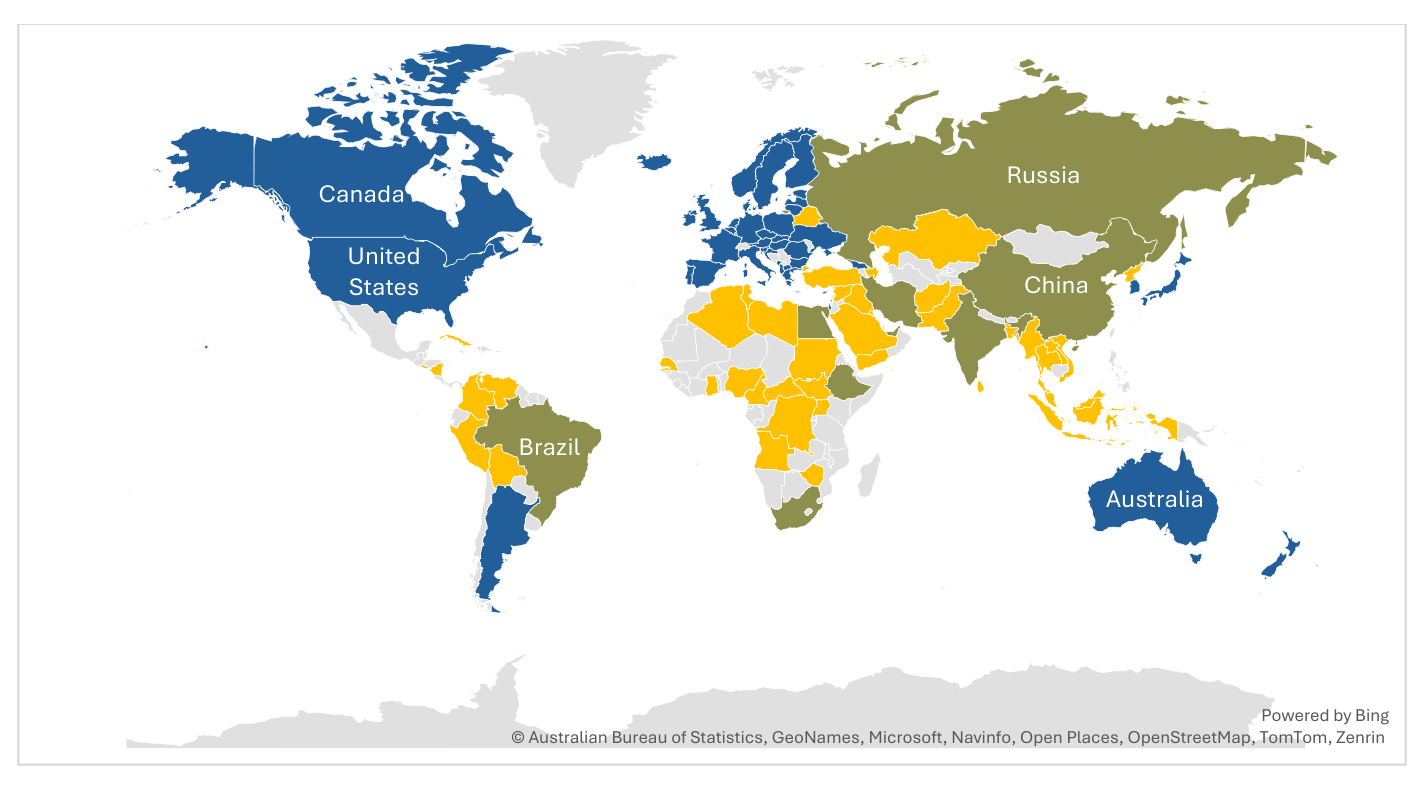

Many countries have expressed interest in or have already applied to join BRICS. One notable example is Turkey, a NATO member that has recently adopted an increasingly anti-Western stance. Turkey's accession to BRICS would represent a significant setback for Western allied forces due to its geopolitical, economic, and military implications. The other countries are mainly from Africa, South America and Asia. Only one country – Belarus is from the European continent which is Russia's closest ally for many years. By 2024, 19 countries have applied to join BRICS while another 21 expressed interests.

| Expressed interest | Region | Officially applied | Region |

|---|---|---|---|

| Angola | Africa | Algeria | Africa |

| Cameroon | Africa | Senegal | Africa |

| Central African Republic | Africa | Zimbabwe | Africa |

| Congo | Africa | Bolivia | Americas |

| DR Congo | Africa | Cuba | Americas |

| Ghana | Africa | Venezuela | Americas |

| Libya | Africa | Azerbaijan | Asia |

| Nigeria | Africa | Bahrain | Asia |

| South Sudan | Africa | Bangladesh | Asia |

| Sudan | Africa | Kazakhstan | Asia |

| Tunisia | Africa | Kuwait | Asia |

| Uganda | Africa | Malaysia | Asia |

| Colombia | Americas | Pakistan | Asia |

| El Salvador | Americas | Palestine | Asia |

| Nicaragua | Americas | Saudi Arabia | Asia |

| Peru | Americas | Turkey | Asia |

| Afghanistan | Asia | Thailand | Asia |

| Indonesia | Asia | Yemen | Asia |

| Iraq | Asia | Belarus | Europe |

| Laos | Asia | ||

| Myanmar | Asia | ||

| Sri Lanka | Asia | ||

| Syria | Asia | ||

| Vietnam | Asia |

If all the proposed countries were to join BRICS tomorrow, it would become the largest political and economic bloc in the world. This expanded BRICS coalition would control more than 50% of global GDP when measured by purchasing power parity (PPP, International $) and encompass approximately 71% of the world's population. Such an entity would not only dominate global economic output but also wield substantial political influence, potentially reshaping the global balance of power and challenging existing international institutions and alliances. The sheer scale of this group could significantly alter the dynamics of global governance, trade, and diplomacy.

In modern times, new challenges have emerged, reflecting confrontations between authoritarian and democratic nations. While the 20th century was defined by an ideological clash—capitalism and freedom versus fascism, communism, and totalitarianism—many believed the 21st century would be dominated by a global fight against terrorism. However, it has become clear that authoritarian countries are aligning themselves in an effort not only to reduce Western influence but also to actively reshape internationally recognized borders and global order. For example, Russia's actions in Ukraine, now with semi support from China, North Korea, and Iran, reflect this trend.

On the other side, democratic nations have seen their global influence wane over the past decades, partly due to policies of accommodation with authoritarian regimes and domestic welfare policies alongside harmful monetary policies that have contributed to reduced wealth creation, noticeable deterioration in the demographic environment, marked by declining birth rates, aging populations, and increasing migration challenges. As a result, the world appears to be returning to a bipolar dynamic, not between capitalism and socialism, but between authoritarianism and democracy. Today, many BRICS countries have extremely different geopolitical interests in general, but against the western dominance, authoritarian model of government can be the key connection between BRICS nations.

There are still numerous challenges facing the BRICS countries, including political instability, lack of property rights in some regions, varying political systems, and internal competition—most notably between China and India. Despite these issues, BRICS nations have demonstrated significant resilience, managing to maintain growth in the face of Western sanctions. Economically, demographically, and militarily, these nations continue to advance. They are also pursuing alternatives to traditional Western financial institutions like the World Bank and IMF. The establishment of the New Development Bank (NDB) is a prime example, with its assets rapidly growing, underscoring the bloc's desire for financial independence and cooperation.

Moreover, the NDB offers these countries a platform to fund vital infrastructure and development projects, bypassing reliance on Western financial oversight. As their economies diversify, the BRICS countries are further exploring regional trade agreements and the possibility of conducting transactions in local currencies, thus reducing dependence on the U.S. dollar. This movement is critical as they seek to insulate themselves from global economic volatility and external political pressures.

While challenges persist, BRICS countries are successfully building alternatives to traditional financial systems and increasing their global influence through economic growth and strategic partnerships. The creation and strengthening of initiatives like the NDB and de-dollarization initiatives showcase their determination to shape a new global financial order, which reflects their interests and priorities.

In the long run, if BRICS continues to strengthen its political, economic, and military cooperation, it could present a significant challenge to the Western-dominated world order. One of the most discussed topics among BRICS countries is the potential introduction of a new single currency to replace the U.S. dollar and reduce U.S. economic influence. Some member states, including Iran, Russia, and China, have already finalized agreements to trade with each other using their local currencies instead of the dollar.

For today, adopting a common currency may seem impossible in recent years, but it is essential to conduct deeper research into the subject to assess how realistic the monetary threat from the East is and what steps the United States can take to prevent the deglobalization of its currency.

Prospects for the Future

In economics, discussing the future is often considered unwise due to the numerous variables and uncertainties, making it impossible to predict outcomes with precision. This is why economics tends to focus more on evaluating the past than predicting the future. The same is in political science. However, there are instances when exploring various future scenarios still may be appropriate. When it comes to the hegemony of the US dollar and its potential challenges, there are only three possible outcomes:

- A gradual loss of dominance

- A more rapid decline

- Maintaining the dominance

Gradual loss of dominance

The gradual erosion of a currency's dominance is closely tied to the diminishing economic strength and declining political power of a nation. Most historical examples of global powers demonstrate that currency issues were among the most significant factors in their loss of global dominance, ultimately leading to either the collapse of the hegemon or substantial weakening.

For instance, after Augustus' monetary reforms in the Roman Empire, the purity of silver coins was around 97-98%. However, over time, to fund rising fiscal demands, waste, and military campaigns, subsequent emperors reduced the silver content, which caused inflation. By around 300 A.D., the silver content of the Roman denarius had fallen to just 2%. Inflation skyrocketed, and the Roman Empire soon fell.

A similar situation occurred in the British Empire. In 1717, the pound sterling was fixed to gold, which kept inflation low. However, during the Napoleonic Wars in the early 1800s, the retail price index rose from 100 to 400. In addition to inflation, the national debt exceeded the size of the entire British economy. Another significant surge in inflation occurred during World War I, when the average annual inflation rate was 15.3%, with a total inflation rate of 75% during the war.

After abandoning the gold standard, high inflation became a persistent issue in the United Kingdom. The history of decolonization and the decline of the British Empire aligns closely with high inflation and the devaluation of the pound sterling. Before abandoning the gold standard, Britain had lower inflation than countries like France, Germany, Italy, and Japan. However, between 1950 and 1993, Britain faced higher inflation levels than many of these nations.

Inflation was the biggest problem faced by the Weimar Republic in the 1920s, particularly between 1919 and 1923. It contributed to the destruction of democracy in Germany and paved the way for the rise of a totalitarian regime, which ultimately culminated in Nazi rule. From 1919 to 1921, inflation was in the double digits, but by January 1923, annual inflation had soared to 2,685%, and by November, it had reached a staggering 750 billion%. Inappropriate monetary policy led Germany into extreme economic depression and facilitated the rise of Hitler and nationalist-socialists within the country.

The first and most realistic, though undesirable, scenario for the US dollar is a gradual loss of its hegemony over time, as has been happening in recent decades. For instance, over the past 25 years, from 1999 to 2024, the average rate of de-dollarization has been -0.51 percentage points per year. This suggests that by 2074, the US dollar's share in global currency reserves could fall below 36%, compared to today's 58% and with wrong monetary, fiscal, trade and foreign policies, political and military dominance also will be downgraded.

With a 36% share in global reserve composition, the United States would still hold the top position. However, this is not just about being first on the list; it's about maintaining hegemony and how widely the currency is used across the world. If current trends continue, and the Federal Reserve and U.S. government maintain the same monetary, economic, and public policies as they have over the past decade, the U.S. dollar will no longer be the dominant global currency within two decades.

To see a clear perspective, we must zoom out and view global events on a larger scale. The United States, a global power, has experienced high inflation rates during various periods, especially after the COVID-19 pandemic and aftermath, which has gradually eroded its dominance. De-dollarization is occurring in a high pace that has not only economic, but mainly political reasons, and without a solid, long-term monetary reform, this concerning trend will persist. In just four or five decades, the United States could not only fall behind many countries economically but also lose its position as a central financial leader.

A more rapid decline

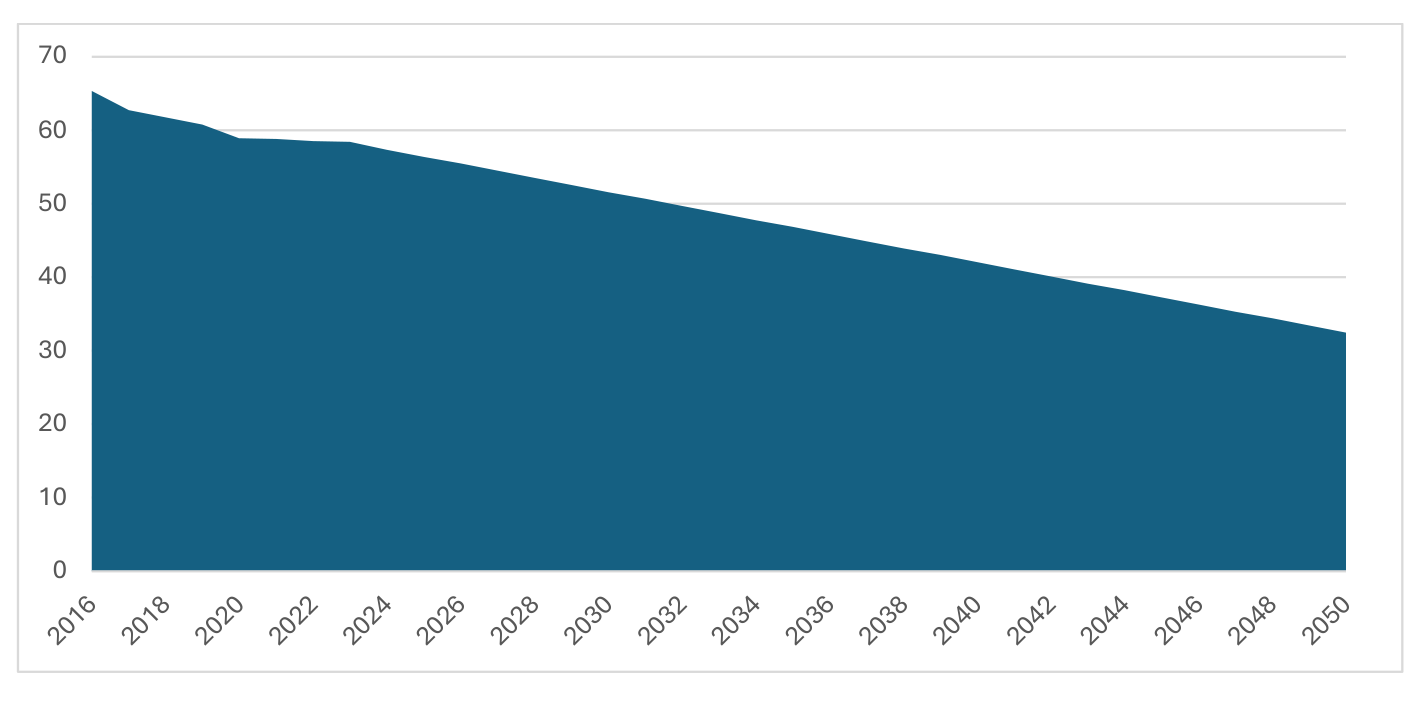

Another potential future for the U.S. dollar is the loss of its hegemony in the medium term, for example, over a 20 to 25-year period. In recent years, unfriendly countries have made efforts to reduce and eventually eliminate their dependence on the U.S. dollar and the U.S. economy as a whole. This trend will likely accelerate the process of de-dollarization, but it is impossible to quantify and translate into numbers this acceleration process or predict the exact rate at which it will occur, and thus, how many years the U.S. dollar has left as the world's leading currency. Political positions and future developments are not easily measurable, and no one can accurately predict the future, especially in economics and particularly with specific numbers. Therefore, it would be more appropriate to examine the past eight years of U.S. dollar hegemony decline and use that as a basis for forecasting the next 20 to 25 years, as this period already contains an observable acceleration rate and trend. From that perspective, by 2050, the U.S. dollar's share of global currency composition could fall to 32%, which is nearly half of today's figure.

As mentioned above, COVID-19 and the war in Ukraine have accelerated the process of de-dollarization, as more authoritarian countries are pushing back against the U.S. dollar. Currently, 43 additional countries have expressed interest in joining BRICS, including some whose currencies are pegged to the U.S. dollar. In addition, in the list of these countries is Turkey, an authoritarian state and a current NATO member. This represents a significant political statement regarding geopolitical shifts, even though there has been no mention of Turkey leaving the North Atlantic Treaty Organization.

Often cataclysmic changes are not a subject of evolution but some bold events that change rules of the game. In our scenario it may be some monetary action from the United States geopolitical foes and economic competitors. To create a strong monetary competitor for the U.S. dollar, several factors must be given into consideration.

First and foremost, a currency can exist for political reasons, not just economic ones. The euro is a prime example. The European Union was formed not only to promote free trade but also for political reasons, particularly to prevent future wars on the European continent. This political motivation was arguably the most important factor. In 1999, the euro was introduced as a single currency, and today, the Eurozone comprises 20 European member states. Currently, the euro accounts for nearly 20% of global currency reserves, making it the second most-held reserve currency after the U.S. dollar. The euro reached its peak in 2009, when it represented 28% of global reserves. Since then, over the past decade, it has maintained a stable rate of around 20% on average.

The second and third essential factors are having of a fiscal union and trust, which comes from an economy with strong property rights. These elements contribute to currency stability and foster trust, making it suitable for use as a reserve by various countries. For example, the EU, while moving slowly, is progressing toward a fiscal union and has a long-standing tradition of property rights and economic cooperation. In contrast, for BRICS, forming a fiscal union is nearly impossible due to a range of factors, from geographical reasons to differing government systems. Additionally, many of these authoritarian regimes have ignored property rights for decades, undermining economic freedoms. What little economic freedom exists often relies on basic bureaucratic procedures, low tax rates, controlled monetary policies, and fiscal discipline that that western countries lack for the last decades.

In recent decades, and especially following Russia's invasion of Ukraine in 2022 and Iran-backed terror attacks on Israel in 2023, it has become evident that authoritarian regimes are increasingly aligning against Western adversaries and adapting to new circumstances at a rapid pace. This suggests that they now have stronger political motivations than ever to create a shared currency or monetary union, and many are already considering it. While they may have the political will, what they lack and will continue to lack are a fiscal union and strong property rights. These are critical, yet unrealistic, factors for establishing a unified monetary regime for those countries. This is where gold comes into play. Gold can act as a substitute for political instability, weak property rights, and unpredictable policies of authoritarian governments. As an asset and a symbol of stability and prosperity, gold could provide the foundation for these regimes to create a more stable monetary system. By adopting gold as a reserve asset and fixing their currencies to it, they could potentially reduce, and eventually end, their dependence on Western currencies and economies.

There are several options for adopting gold, but the two most realistic scenarios are either establishing a BRICS single currency backed by gold or adopting a gold standard for the Renminbi, with other BRICS member states pegging their currencies to it (similar to the Bretton Woods system). BRICS countries, both current and potential members, already account for 50% of the world's reserves, significantly surpassing Western countries, and this number continues to rise each year. Although their economies represent only 34.7% of global nominal GDP, there would likely be no issue in terms of gold reserves to support adjusting their currencies to this asset.

Adopting a single BRICS currency would require all member countries to relinquish their individual monetary policies, transform their central banks into a unified monetary authority, and adopt common centralized tools and policies with shared constraints. Given the number of authoritarian regimes involved, this approach is highly unrealistic at present, as surrendering such significant power is not typical in authoritarian countries. Moreover, these nations have varying fiscal policies, which would further complicate the implementation of a unified currency.

Considering the arguments above, a more realistic gold-based solution would be to establish a system similar to Bretton Woods, where the Renminbi is backed by gold, and other countries peg their currencies, either fully or partially, to the Renminbi. These countries would use the Renminbi for all international trade, investment, and other financial activities. This approach does not require full consensus among BRICS countries; it would be sufficient for a majority to join the new 'Renminbi Area,' like the Eurozone. The success of the 'Renminbi Area' would likely determine whether additional countries choose to join.

If BRICS countries successfully implement such a policy, and the U.S. dollar continues to have inflationary record and is used as a political tool, the global monetary landscape could shift. As the dollar becomes less reliable for some nations, more countries will be motivated to seek alternatives and align with those offering more stable and trustworthy monetary regimes. This could lead to an increasing number of nations distancing themselves from the U.S. dollar and band-wagoning with countries that demonstrate stronger financial stability, reducing their dependency on Western currencies in favor of new, more predictable systems.

Maintaining the dominance

In the current era of de-dollarization, halting or reversing the global trend is becoming increasingly challenging. Nevertheless, if the U.S. government seeks to preserve its economic, financial, and political dominance, the Federal Reserve must prioritize tightening monetary policy and implementing long-term strategies. These strategies should focus on fostering sustainable economic growth rather than being swayed by short-term economic or political objectives. To complement these efforts, the federal government must reduce its fiscal demands, starting with a rapid reduction in the budget deficit. Furthermore, it is critical that the government refrains from relying on Federal Reserve policy to finance its liabilities, as such actions undermine the long-term stability of the U.S. economy. A disciplined approach to both fiscal and monetary policy is essential to maintaining investor confidence and ensuring the U.S. remains an attractive destination for global capital, even in the face of the de-dollarization trend.

The primary mission of all currencies worldwide is to ensure price stability. This is the central function of every country's central bank. To slow the pace of de-dollarization, the first priority is to maintain a minimal or no inflation at all (nearly zero). Achieving this requires depoliticizing the Federal Reserve and implementing a strict monetary policy that adjusts interest rates and applies quantitative tightening whenever necessary, not just when politically convenient.

To demonstrate its commitment to fighting inflation and restoring sound monetary policy, the Federal Reserve should cease financing the federal budget by purchasing Treasury securities. A legal ban on this practice would send a strong signal to the market that the Fed is serious about controlling inflation. Another tool to combat inflation is not only raising the policy rate but also keeping it higher than the supply-demand equilibrium rate, ensuring that commercial banks borrow from the Fed only when they have a critical need for liquidity. While there are more transformative approaches to overhauling the system, such as reintroducing the gold standard or even abolishing the Fed, addressing specific monetary policy reforms requires more in-depth research.

There are more policy tools that affect the confidence in the U.S. dollar and fiscal policy is the second most important after monetary policy. First of all, reduction the budget deficit is crucial to borrow less and in best scenario not to borrow at all from the Federal Reserve. As mentioned earlier legal ban on this instrument will be a bold step towards fixing the system. Secondly, reforming tax system so that saving and investment to be encouraged will greatly affect currency stability and confidence. Fewer and less taxation means more saving and investment.

Another key area for reform is trade. Expanding trade partnerships and pursuing both bilateral and multilateral free trade agreements will help promote transactions in U.S. dollars. Trade wars, such as the one with China in 2016, ultimately weaken the U.S. currency by encouraging other countries to seek alternatives and reduce their reliance on the U.S. dollar. It is essential not only to promote free trade with other nations but also to implement a corresponding energy policy. The more the United States trades its natural resources, the greater the dominance of the U.S. dollar over other economies. For example, in recent years, Russia has denominated its energy prices in Russian rubles, using this strategy as a tool to counter dollarization.

In conclusion, implementing strict monetary and fiscal policies, along with reforms in trade and regulatory frameworks, is crucial to achieving greater economic freedom. Such freedom is not only the cornerstone of sustaining long-term, high GDP growth but also essential for attracting global investment back into the country and enhancing overall economic capabilities. These reforms have far-reaching implications across various sectors, and each area requires comprehensive analysis, strategic planning, and targeted research. While it is clear that a holistic approach encompassing fiscal responsibility, trade openness, and regulatory efficiency is necessary, this paper specifically focuses on the monetary capabilities of the United States. Future research should dive deeper into these interconnected areas to provide a more detailed roadmap for strengthening the U.S. economy and reinforcing its global financial leadership.

Conclusion

The hegemony of the US dollar emerged from several historical factors. It began with the gold standard, which did not imply strict monetary policy but rather the absence of one. During this period, the US dollar experienced decades of appreciation and general price level reduction, driven by industrialization and technological progress. However, wars and the growing size of government eventually made the gold standard incompatible with political and economic policies of the government. However, after World War II, the United States and its allies adopted the Bretton Woods system, a weaker version of the gold standard, which formally recognized the US dollar as the world's leading currency. After that, the collapse of the Soviet Union and communism in the early 1990s further solidified the United States' status as the sole global superpower, reinforcing the dominance of the US dollar by providing stability, fostering future economic development, and strengthening international trust in the currency not for the monetary, but for the political reasons.

In the late 20th and 21st centuries, the United States has faced growing challenges from China, Russia, Iran, and other authoritarian governments. These nations have even formed a coalition called BRICS, aimed at reducing Western dominance over Asian, African, and South American nations. Many more countries are eager to join BRICS and including them the coalition will represent 71% of the world's population and 50% of the global economy (in PPP, current international $). Their primary goal is to diminish Western influence, allowing them to operate without dependence on liberal-democratic nations, freeing them to pursue inhumane and ruthless policies that secure the future for their authoritarian leaders, while creating hardship for masses living in their countries.

The weakening dominance of the US dollar opens the door for the rise of authoritarian regimes' currencies, such as the Chinese renminbi and the Russian ruble. Every space left by the retreating United States will be filled by growing authoritarian influence. Ultimately, this shift poses an existential threat not only to neighboring or regional nations of the authoritarian countries but to any global competitors, including the United States, European Union, Japan and others.

The implications of the shift in currency dominance will be far-reaching. The US dollar has long served as the world's primary reserve and trade currency, providing the United States with lower borrowing costs and significant geopolitical leverage. However, this status is now under threat due to the accelerating process of de-dollarization. This trend is driven not only by the rise of authoritarian governments but also by poor policy decisions made by the Federal Reserve and the US government. Years of expansionary monetary policies have led to inflation, increased market volatility, and a growing lack of trust in the US dollar.

The responsibility for this lies in inflationary monetary practices, deficit spending, declining economic freedom, and weakened foreign policies. These factors have contributed to the erosion of confidence in the dollar, intensifying the global shift away from US currency dominance.

The de-dollarization process is advancing rapidly to the point where it can no longer be ignored by US policymakers. The world is shifting towards a multipolar order, like the Cold War era and earlier times when long-lasting peace and prosperity weren't options at all. In those periods, trade and finance were not global phenomena; instead, nations pursued nationalist policies, closing borders, embracing mercantilism and protectionism, and increasing military expenditures. This is not the kind of world that American or European citizens are accustomed to for the last decades, nor are they prepared for a new Cold War especially one with geopolitical adversaries far more complex and powerful than the Soviet Union and its communist allies.

There are three possible scenarios for the future of the U.S. dollar: (1) a gradual loss of dominance, (2) a more rapid decline, and (3) maintaining the dominance. All else being equal, a gradual loss of dominance seems inevitable, as this process has already been underway for years, driven by the ongoing de-dollarization efforts of other nations, especially China, Russia and Iran. However, if additional factors such as geopolitical developments, actions by the Federal Reserve and U.S. government, and the policies of authoritarian BRICS regimes are considered, a more rapid decline in the dollar's dominance becomes increasingly plausible.

BRICS countries have several options to accelerate this process, such as introducing a gold-backed single currency or establishing an "Asian Bretton-Woods" system, in which the Chinese renminbi would be backed by gold, with the currencies of BRICS members and potential partners pegged to the renminbi. While other monetary scenarios are possible, achieving and sustaining currency dominance requires both fiscal union which is unrealistic for many reasons, especially geographic ones, and strong property rights - the element currently lacking in all the authoritarian states. To compensate for the absence of these, gold could serve as a substitute, as it has a long history of providing stability and success in monetary policy. Moreover, BRICS nations have accumulated gold reserves that exceed their share of the global economy and continue to increase their holdings, reducing their reliance on the U.S. dollar.

The third scenario - maintaining the dominance of the U.S. dollar would be very difficult to achieve without significant changes in the United States' monetary, fiscal, regulatory, trade, and foreign policies. While this paper focuses primarily on monetary policy, it is important to recognize that all these areas are interconnected. The Federal Reserve must adopt the policies that ensure price stability in a long run. For this it is essential for the monetary authority not to use its power for political purposes and must not finance the government as well as must stop subsidizing private sector through commercial banks. A strong and dominant currency requires not only a strong monetary policy, but a high degree of economic freedom within the country to ensure sound money and to attract global investment and foster high economic growth. With these conditions in place, the U.S. could potentially reverse the current trend of losing its leading role in the global economy and politics.

The future of the dollar's hegemony will depend on how effectively the US responds to the challenges mentioned above. While BRICS countries are not yet successful in replacing the dollar as a hegemon currency, their growing economic influence and coordinated efforts to challenge the status quo suggest that US policymakers must be prepared for more push from the authoritarian governments in promoting their monetary and therefore political agenda. Failure to do so may result in a gradual erosion of the strategic and economic benefits that the US has long enjoyed.

Data & sources

The paper draws on primary data from the International Monetary Fund (COFER currency-composition data and the AREAER exchange-arrangements report), the World Bank (World Development Indicators), the Federal Reserve (FRED and the H.10 exchange-rate release), the U.S. Bureau of Labor Statistics (CPI), the Atlantic Council's Dollar Dominance Monitor, and the World Gold Council. It also engages the work of John B. Taylor, Allan H. Meltzer, Milton Friedman, Francis Fukuyama, and Foa and Mounk, among others. The 52 numbered references below give the full citations.

How to cite

Endnotes

- Hanna Arhinova and Tassanee Vejpongsa, "Ex-Ukrainian president says US delay in war aid was 'colossal' waste, let Putin inflict more damage," Associated Press News (May 14, 2024).

- Atlantic Council, "Dollar Dominance Monitor" (2024), atlanticcouncil.org.

- Chinese Cross-Border Interbank Payment System (CIPS).

- Society for Worldwide Interbank Financial Telecommunication (SWIFT).

- International Monetary Fund, "Currency Composition of Official Foreign Exchange Reserves (COFER)" (September 27, 2024), data.imf.org.

- Bureau of Labor Statistics, "Consumer Price Index (CPI)" (2024), bls.gov/cpi; Robert Sahr, "Historical Study," Oregon State University (2018).

- Ibid.

- Roberto S. Foa, Margot Mollat, Han Isha, Xavier Romero-Vidal, David Evans and Andrew J. Klassen, "A World Divided: Russia, China and the West," Centre for the Future of Democracy, Cambridge (October 2022).

- Federal Reserve System, "Foreign Exchange Rates" – H.10 Weekly (2024), federalreserve.gov.

- Milton Friedman, "Money, Credit and Banking Lecture" (1982).

- John B. Taylor, "Monetary Policy Rules Work and Discretion Doesn't: A Tale of Two Eras" (2012).

- Federal Reserve Bank of St. Louis, "FRED Economic Data" (2024), fred.stlouisfed.org.

- Ibid.

- Ibid.

- Ibid.

- Allan H. Meltzer, "What's Wrong with the Federal Reserve: What Would Restore Independence?" (2013).

- Peter C. Earle, "Book Review: 'Paper Soldiers: How the Weaponization of the Dollar Changed the World Order,'" Quarterly Journal of Austrian Economics 27 (2024).

- World Bank, "GDP Growth (annual)" (2024), data.worldbank.org.

- Peter C. Earle, "De-dollarization Has Begun" (April 11, 2024), aier.org.

- Francis Fukuyama, "The End of History?" The National Interest, p. 17 (1989).

- Vladimir Putin annual state of the nation address to parliament; the collapse of the Soviet empire "was the greatest geopolitical catastrophe of the century" (April 25, 2005).

- World Bank, "GDP, PPP (Current International $)" (2024), data.worldbank.org.

- World Bank, "GDP (Current US$)" (2024), data.worldbank.org.

- Centre for Research on Energy and Clean Air, "Financing Putin's War: Fossil fuel imports from Russia during the invasion of Ukraine" (2024), energyandcleanair.org.

- Ibid.

- Atlantic Council and World Gold Council, "Dollar Dominance Monitor" (2024).

- World Gold Council, "Gold Reserves by Country," author's calculations (2024), gold.org.

- Maia Nikoladze and Mrugank Bhusari, "Russia and China Have Been Teaming up to Reduce Reliance on the Dollar" (February 22, 2023), Atlantic Council.

- Markets – Business Insider, "The BRICS summit ended with no new currency and all 5 members issuing differing and contradictory commentary on de-dollarization" (August 28, 2023).

- Vasuki Shastry, "Without a Viable Alternative, Dollar Dominance Upsets Emerging Markets" (May 11, 2023), Forbes.

- Stefan Gleason, "BRICS Countries Planning New Gold-Backed Currency" (July 10, 2023), Money Metals.

- Joe Sullivan, "A BRICS Currency Could Shake the Dollar's Dominance," Foreign Policy (April 24, 2023).

- Voice of America News, Saibal Dasgupta, "BRICS meeting highlights geopolitical aspirations, rivalries with West" (October 24, 2024).

- Ibid.

- International Monetary Fund (IMF), "Annual Report on Exchange Arrangements and Exchange Restrictions" (July 26, 2023).

- European Parliament Briefing, "Expansion of BRICS: A quest for greater global influence?" (March 15, 2024).

- Canada, United Kingdom, European Union, Japan, Korea Rep., Australia.

- Countries that expressed interest or officially applied for joining BRICS.

- World Bank, "GDP, PPP (Current International $)" and "GDP (Current US$)" (2024).

- Yascha Mounk and Roberto Stefan Foa, "The End of the Democratic Century: Autocracy's Global Ascendance," Foreign Affairs, Vol. 97, No. 3 (May/June 2018), pp. 29–36.

- Roberto Stefan Foa, Yascha Mounk and Andrew Klassen, "Why the Future Cannot Be Predicted," Journal of Democracy, Vol. 33, No. 1, pp. 147–155 (January 2022).

- A.H.M. Jones, "Inflation under the Roman Empire," The Economic History Review, Second Series, Vol. V, No. 3 (1953).

- Pat Heller, "The Lasting Legacy of the Roman Denarius" (May 23, 2019).

- Matthew Heckel, "Inflation and the Fall of the Roman Empire" (2018), Federal Reserve Bank of St. Louis.

- Helen MacFarlane and Paul Mortimer-Lee, "Bank of England Quarterly Bulletin: Inflation Over 300 Years" (May 3, 1994).

- Helen MacFarlane and Paul Mortimer-Lee, "Bank of England Quarterly Bulletin: Inflation Over 300 Years."

- Lewis E. Hill, Charles E. Butler and Stephen A. Lorenzen, "Inflation and the Destruction of Democracy: The Case of the Weimar Republic" (June 1977).

- International Monetary Fund, "Currency Composition of Official Foreign Exchange Reserves (COFER)," and author's calculations.

- Ibid.

- Francesca Spigarelli and Nikolai G. Wenzel, "Monetary Union Without Fiscal Union? The Euro Crisis and the Move Towards European Fiscal Union," New Perspectives on Political Economy, Vol. 11, Nos. 1–2 (2015).

- Yascha Mounk and Roberto Stefan Foa, "The End of the Democratic Century: Autocracy's Global Ascendance," Foreign Affairs, Vol. 97, No. 3 (May/June 2018), pp. 29–36.

- James D. Gwartney, Robert A. Lawson and Randall G. Holcombe, "Economic Freedom and the Environment for Economic Growth," Journal of Institutional and Theoretical Economics (JITE), Vol. 155, No. 4 (December 1999).